Welcome back,

I took a few days off (still not quite at my usual cadence) not to annoy my American readers who have been celebrating Independence Day and spending more time with family. However there are some urgent developments worth mentioning briefly. A lot of American trends are demonstrating some issues with AI actually not boosting productivity.

In my opinion a major change has taken place in June, 2026. Let me try to explain. On June 12th, 2026 the U.S. government abruptly restricted Anthropic’s Mythos class of models. This among other related things has significantly broken down trust in closed-source models and companies like Anthropic and OpenAI. It’s a big shift.

If 2025 was the year where vibe coding failed to contribute meaningful products at scale, 2026 is the year when tokemaxing led to high Claude code bills and became token-minimization where AI agents failed to demonstrate as much value as it was hoped that they would at some of the biggest and most powerful companies. This has predictably led to more widespread adoption of open-weight models out of China. This is a marked change for the future of AI and illustrates how AI has rising elements of class struggle, geopolitics, AI policy impacted risk mitigation and a problematic declining public perception and negative sentiment towards AI.

I’ve never seen such division in the AI community over closed source vs. open-source models before as I have in the weeks near the end of June, 2026. A world where the U.S. government not only puts Anthropic on a supply-chain risk sanction list (back in February) but restricts their breakthrough Mythos class of models. Where Palantir, a company embedded within the Pentagon and U.S. administration is openly questioning the value proposition of Anthropic and closed-source model makers. This made me very uncomfortable because you have someone embedded in the National defense complex making an argument for open-weight models that China currently dominates.

2 Minutes 49 seconds Clip – Alex Karp CEO of Palantir

While Palantir has business reasons to make this argument1 (since Anthropic is likely a direct Enterprise AI competitor), to watch the Pentagon and Palantir (who are supposed to be protecting American interests) hurt the AI leadership of America with brash arguments that favor China and Chinese AI products is very disconcerting and drankly disheartening.

This is leading to a big transfer from closed-source models to open-source models that will make some of China’s AI startups way more profitable. Many businesses can’t work with AI companies that are restricted or whose models can be shut down at any time, and who are as expensive as Mythos (Fable 5) models are relative to the competition. Businesses have had to pivot. The Trump Administration have significantly damaged America’s AI leadership in the past few weeks.

Meanwhile, the build out of AI infrastructure is not slowing down, it’s speeding up.

The Mega Neo Clouds are Arriving in 2026

In early July, not only has SpaceX but now Meta and Softbank (via SB Neo) have entered the Neo Cloud arena of selling compute and developing massive datacenters with an aggressive monetization plan.

Google, Amazon, Microsoft and others could follow suit to generate more revenue that appeases shareholders worried about declining free-cash-flow and mounting debt. It also accelerates a race to orbital compute (datacenters in space).

Google’s planned Neo Cloud with Blackstone is actually already doing this with their TPU Cloud announced on May 19th, 2026.

These Token Apocalypse and Mega Neo Cloud movements intensifies the dynamics at play in AI’s roll-out and the market bubble around semiconductors and related to the datacenter push and how incumbents and hyperscalers respond. If Meta becomes a Cloud computing hyperscaler in their own right it fundamentally changes the future. More routing of Chinese models also means China’s public markets where many startups have gone public is super-charging China’s AI development.

Whether you believe in DeepSeek moments, you could make the argument that DeepSeek’s open-source progress of early 2025, a moment that began on January 20th, 2026 with DeepSeek-R1’s release, led to a second DS moment with Manus AI2 and now a third with Zhipu’s GLM 5.2. of June 16th, 2026. All of these factors are changing the history of AI. While you’ve been away, it’s a been a busy summer in the macro picture of Generative AI.

The Pentagon formally designated Anthropic as a “supply chain risk” on February 27, 2026. The Trump Administration is directly responsible for some of the pivot of American companies and Enterprises pivoting from Claude models to Open-weight Chinese models. The setup of course to the Token Apocalypse, whereby companies are radically minimizing token spend of employees had to do with a narrative that AI agents could boost productivity.

The peak of “tokenmaxxing”, this suspicious trend in Silicon Valley where a workplace culture frenzy of burning through as many AI tokens as possible as a shorthand for productivity—ran into a major reality check sometime in the early spring of 2026 when they got the Claude bills. The adoption of Chinese open-weight models coincided with the reaction to that.

This is actually a failure of AI agents and productivity if you read between the lines. Last Thursday Mark Zuckerberg told Meta employees at an internal town hall that AI agent development has not accelerated as quickly as he expected. Suddenly companies and Enterprise level businesses are rationing their token use alarmed by how much their AI (mostly Anthropic) bills ballooned.

The Transition to Open-weight Models and Routing has Accelerated meaningfully in mid 2026

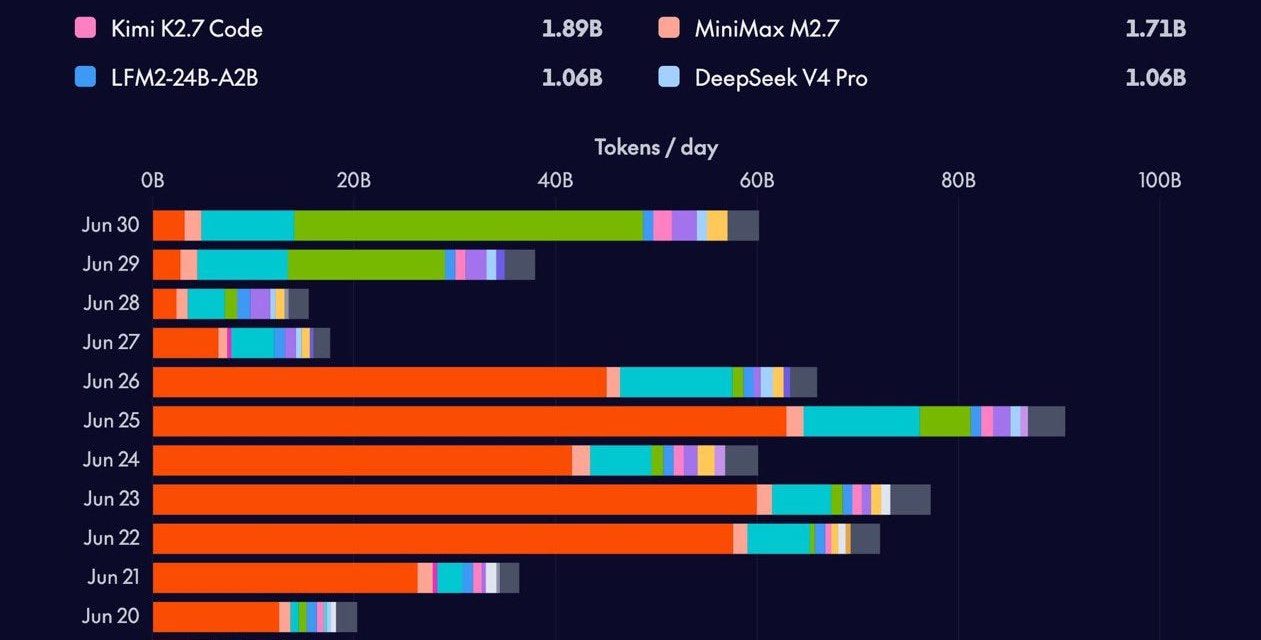

This is also setting the stage for American open-source winners. Nvidia’s Nemostron is such an example: Nemotron doing 35B tokens all of a sudden:

In a world of more token usage and inference, Open-weight models gain in relative value and competitiveness. Cost to performance becomes more of a factor.

The Token Apocalypse is that crucial moment where companies realize switching to Chinese open-weight models or open-source models made in the West has become a business necessity to get the most of AI agents without breaking the bank. I believe July, 2026 is that moment. If I’m right, at the scale we are going to see this trend, it could have a material impact on slowing down the growth of AI behemoths and model makers like Anthropic, OpenAI, Google, SpaceX, Meta and others. That is also a big deal for the AI bubble.

This third Deep Seek Moment of Zhipu AI’s GLM 5.2 performing so well, changed the fundamental economics around token usage. With the highest level of Mythos class models being restricted, it no longer made sense to keep using Closed-source models all the time but only for special projects. The vast majority of business or personal use cases do not require bleeding edge models.

To make matters worse on the Trump Administration side and the Palantir (pro-China) statements, another one of their co-conspirators Sam Altman offered the Trump Administration to take a 5% Government stake in OpenAI. The topics look very bad for OpenAI courting Trump (who is famous for accepting bribes and trading favours), and for the U.S. Government’s involvement in picking the winners in AI at large. Sam Altman, has argued that giving the US public a financial stake in the company is the best way to share the benefits of AI, according to the Financial Times. Obviously those aren’t the real motives for Sam Altman to do this.

The Trump Administration’s directives are seeking to have power over how America’s so-called AI leaders release their models and how they do so. All of which is further enhancing and accelerating the adoption of China’s open-weight models in the business community. This is exactly not how you keep America ahead in AI you might realize. Suffice to say that Palantir and OpenAI’s proximity to Trump is having a harmful impact on their public perception given how unpopular Trump is over the U.S. economy in particular jobs, inflation and his handling of geopolitics, trade and the relationship with U.S. allies. Now with AI’s inflationary impact coming with higher consumer electronics goods like Apple devices, higher electricity prices and less human culture and original IP on the internet, citizens and consumers alike, I would say society and a lot of people are furious.

If you wanted to undermine America’s leadership like the Anthropic’s IPO, this would be how to do it. The statements of people like Alex Karp, Mark Zuckerberg and Sam Altman are highly concerning because they insinustate a world where using Chinese open-weight models is better. This Token Apocalypse have geopolitical and reputational damage for the AI industry. A world where even absurd token spend on AI agents isn’t boosting productivity in a meaningful way. OpenAI offering a 5% stake to the Trump Administration is seen as a precursor of a bailout for their failed AI products while they burn investor funds at unprecedented levels.

The Silver Angle of Sovereign AI Diplomacy

This boosts the prospects of open-weight model makers in America perhaps like Reflection AI, Nvidia, Europe’s Mistral, Canada’s Cohere, among others. Companies want to use efficient cheap models, just not necessarily from China3. The Token Apocalypse also demonstrates a world where model makers are just part of the ecosystem and no longer have the privilege they once had. The description of Coinbase on how to minimize and cut back on Token usage, has become a signal of the Token Apocalypse, that could impact the AI bubble but is also an inevitable push for more efficiency and utility of the technology. Companies are now trying to position themselves as agnostic Sovereign AI intermediaries for the future.

Palantir is partnering with Nvidia in a strategic partnership to deliver secure “Sovereign AI” and operational AI solutions, primarily for U.S. government agencies, critical infrastructure, and allied enterprises. Nvidia’s primary flagship family of open-weight AI models is called Nemotron.

More Notes on the Token Apocalypse

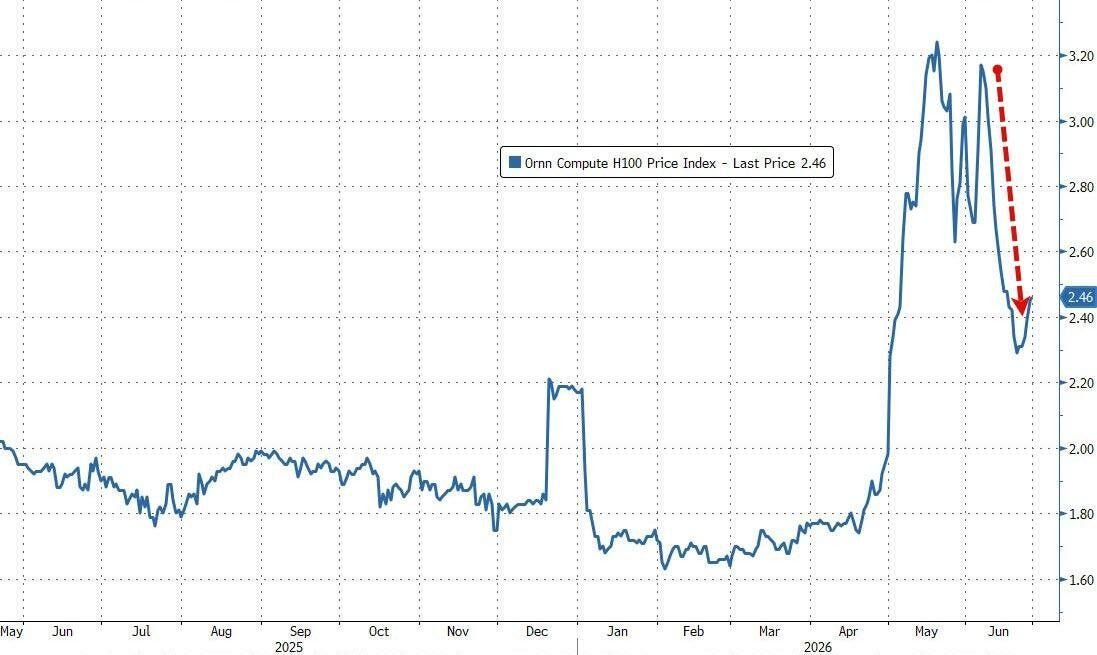

As the demand for compute accelerates exponentially, momentum of LLM API tokens and over-pricing by leaders has meant we’ve entered price-war territory in a pull back from the spike that resulted from tokenmaxxing. Since early Spring, the LLM Token Expenditure Index is (by price) is down 20% from its May high. This insinuates more open-weight model adoption and more routing in general as the new norm.

If the model is no longer the product, what comes next? In a reality where what used to be a premium tech product is quickly turning into a commoditized utility some of the incredible ARR growth that we’ve been used to seeing from Anthropic and OpenAI might start to slow down considerably. And importantly, what does that do to Anthropic and OpenAI’s ARR growth just as they are about to go public?

Overall according to JPMorgan research tracking aggregator data, total LLM token volume surged by 70% month-over-month (May to June), heavily outperforming previous months. Jevons paradox is pushing us to to cheaper more efficient Chinese open-weight models. But with better practices we’ve come a long way from the Tokenmaxing of when Anthropic’s ARR was really accelerating. Given that only a few hundred thousand people in 2026 (mostly at Tech companies) use AI agents at scale with unlimited token budgets and along with the push for physical AI, you can imagine how much the demand for compute is going to continue to spike in the months and the years ahead. Unless you are the leading frontier model like Mythos, your API might not be much in demand compared with Chinese open-weight models.

Token Volume, Jevons Paradox, Without Mythos Access

The Token apocalypse is therefore also simply a scenario where while overall token volume has exploded, U.S. model providers are facing intense volume pressure from low-cost alternatives. That Mythos-class models are priced at a significant premium compared to the rest of the market (*and heavily guard-railed as Mythos 5 and Fable 5) while we don’t even have actual access to the real step-up of Mythos fully without unreasonable constraints, it’s hurting Anthropic’s reputation among users and customers.

My understanding of this situation isn’t perfect, but I wanted to give you a lens in understanding some of what is happening with my own commentary and opinionated viewpoint. The Pentagon and the Trump Administration shouldn’t be penalizing America’s best AI company if the U.S. wants to win against China. Just as it’s inappropriate for a National Defense executive like Karp to be making arguments for open-source models currently dominated by China! It’s shocking really and it shows the Trump Administration is trying to favor plays like OpenAI and Palantir in the process.

In 2026 access to Mythos is incomplete and a caste system around access to frontier models might be on the doorstep. In BigTech engineers at some of the most profitable companies in the world had an incredible access to (nearly unlimited) tokens earlier this year, but the experiment didn’t work out quite as planned. If you have to bend the knee to the surveillance apparatus to be granted access, that is, in the Token Apocalypse major frontier AI labs have begun introducing identity verification (IDV) gates for API and model access – if you aren’t a U.S. citizen and you have high-risk profile, you might be denied access. This is going to make the United States incredibly unpopular in the world at large.

How the GPU Melts Awake

AI compute prices are declining aggressively before major AI IPOs have taken place. So for instance AI compute by the cost to process a fixed amount of data (like a million tokens) is declining of course as well. Open-source competition drives the raw compute (specifically per-token inference) down.

This has the potential to squeeze the margins of foundational model providers and Neo Clouds, both. The decline in private credit funding has forced them to switch from heavily subsidized subscription pricing to token based billing. But this has predictable consequences. Corporations and Enterprise customers are realizing LLMs are way more expensive than they were led to believe. This can challenge trust in the Generative AI narrative for real world efforts where and when enterprises move from a small pilot to full production, they discover that the “total cost of ownership” is massively higher than they anticipated and budgeted for.

How the Tokens Burn 🔥

If we come to a point of sustained lack of ROI from huge token budgets, we’ll start to see the key customers of AI model makers pull back. The evidence of this might come in the form of deterioration in the cash flow of the AI sector’s prospective customers (according to the FT). Their efforts with AI might be expensive but the ROI won’t be showing up in their own Earnings yet, or not at all.

If you believe in the AI bubble crashing, look for a growing divergence between the financial health of the tech companies building AI and the non-tech sectors expected to buy it. For ROI to occur in AI adoption, your customers need to see the benefit. In my mind there’s a disconnect in 2026 where while the US tech sector has seen a sharp re-acceleration in earnings growth (climbing toward 50% YoY), the AI-adopting sectors have seen their earnings growth flatten out and begin to decelerate, hovering just above 0%. That’s generally considered a red flag. So my Token Apocalypse metaphor has multiple meanings, and I hope you enjoyed the exploration.

Models are improving and tokens are getting cheaper, but there’s not much tangible evidence AI is uplifting us.

Thanks for reading!

Alex Karp, CEO of Palantir did say a lot of interesting things in the interview, it’s worth a watch.

The 2nd “DeepSeek Moment” was March 6th, 2026 when Manus AI was released. This company was later acquired by Meta and the decision was reversed by China authorities.

The CEO of Mistral, Arthur Mensch gave really great context on this here as well.

Read More in AI Supremacy