[[{“value”:”

June 25, 2026.

Good Morning from typhoon drenched Taichung, Taiwan. I try to give my readers broad exposure to AI’s evolution from multiple angles. There’s a surprising number of aspects to this.

AI definitely doesn’t move as fast as you think, just take smart cars and autonomous vehicles. Even the best companies doing this in the world are taking decades to scale.

-

On the topic of Physical AI there are the frontiers and then there’s the reality. An important part of how we as consumers experience AI in the physical reality is going to be autonomous vehicles (AVs).

-

Let’s be real, difficult more physical manifestations of AI and emerging tech like AVs, robotics, humanoids, Quantum computers with millions of qubits and even more speculative ideas like datacenters in space are going to be exceedingly difficult to turn into reality. They will on the whole take more time, be slower to arrive and be less capable than you think. Innovation is hard, and God knows we’ve been patient. [The idea that AI is moving so fast isn’t empirically correct]. I’d like to see us cover AI with more realism.

-

Think about how long it’s taken even Waymo to arrive at this point. Waymo was originally founded in January, 2009. On June 11th, 2026 Waymo finally launched a premier subscription tier for $29.99 a month in select cities (called Premier). It’s starting this year in select cities such as San Francisco, Los Angeles and Phoenix. In terms of AV startups, I’m also really bullish on Wayve, an Nvidia backed UK based startup who are building AV based software and AI models for autonomy.

What’s your taxi ride preference? 🗺️

Driver or no-driver, consumer preferences might shift radically in the years ahead. If price wasn’t a factor what would you use?

Physical AI is Hard, Autonomy is Tricky

AVs and robotaxis are still years away from scale and while some of us have experienced them, most of us still have not. The build out of physical datacenters and AI Infrastructure at scale is hitting a crazy number of bottlenecks. Manifesting AI in the real world is just incredibly challenging. By the time we arrive in the 2030s however it’s going to be pretty exciting. Autonomous vehicles (AVs) and Robotaxis have to be one of the most fascinating case studies of this. As will another industry I’m also becoming pretty obsessed with, space-technologies.

Today’s article is going to be primarily about Waymo. I also want to introduce you to some of the AV and mobility related Newsletters I follow.

Harry Campbell of the Driverless Digest Newsletter shared this image recently:

Besides Waymo, there are many other interesting names. There’s the likes of (Amazon’s) Zoox and Mobileye who are also making headway and bigger plans in the Robotaxi direction. Intel majority owned Mobileye is aiming for and initial 100-vehicle fleet into a major U.S. city in 2027 and hoping to scale the fleet to roughly 17,000 vehicles over the next five years.

Google spin-off Waymo is however the outright leader, with a $16 Billion funding round earlier this year and a valuation of over $126 Billion. Alphabet’s stake in Waymo is estimated to be likely well over 70%. So when we say Google is a full-stack AI company – we aren’t just talking vertical integration and the application layer but the most tangible things like transportation and TPUs, the nuts and bolts. All of this is compounded by how well Google has raised capital in 2026. Autonomy and AI infrastructure are just two areas where Alphabet’s future is exceedingly bright.

Waymo will be taking on Uber in its own way but have several global rivals such as Baidu Apollo (Apollo Go), Pony.AI, WeRide, Tesla and a host of others. In March, Uber announced a massive partnership to invest up to $1.25 billion through 2031 to deploy up to 50,000 fully autonomous Rivian R2 robotaxis exclusively on the Uber platform. There are so many players and so many partnerships, it’s a bit confusing even for us who watch the space. How will Waymo challenge Uber and how will all of these partnerships pan out in different regions of the world?

Waymo’s track record is also fairly stunning when it comes to the driver and passenger saftey aspect: Even as Waymo has scaled into increasingly complex environments like airports and new cities, the safety benefits kept compounding. It’s a good sign for the AV industry. While there’s always the funny or scary story of some headline mishap, for the most part the tech is improving.

Waymo is marketing itself a bit like the Anthropic of the road, and as being 10x safer than an average human driver. It certainly makes you pause and wonder.

In case you are interested in following autonomous vehicle news one of my favorites is . I asked him to do a deep dive for us on Waymo, todays’ piece.

The AV Market Strategist

-

Deep Dive Pony.ai: Business Model, Unit Economics, Fleet Data, Financials and More

-

WeRide Hits Madrid, Tesla’s Map Grows but Its Fleet Doesn’t, NVIDIA Wants to Be the Robotaxi Standard

-

Waymo’s Shocking Data Release, Uber Invest $100M in Robotaxi Infrastructure

-

Mobileye Joins the Robotaxi Race

-

Waymo’s Master Plan

So what does a Waymo look like from the inside?

Autonomous AV and Neo Mobility Newsletters of Note ✇

Check out some of the community Newsletters for this topic:

I don’t know what the future holds but there’s probably going to be a Waymo in it.

Let’s get on to our deep dive now by Daniel.

Waymo: The Company That Solved Self-Driving and Now Has to Scale It

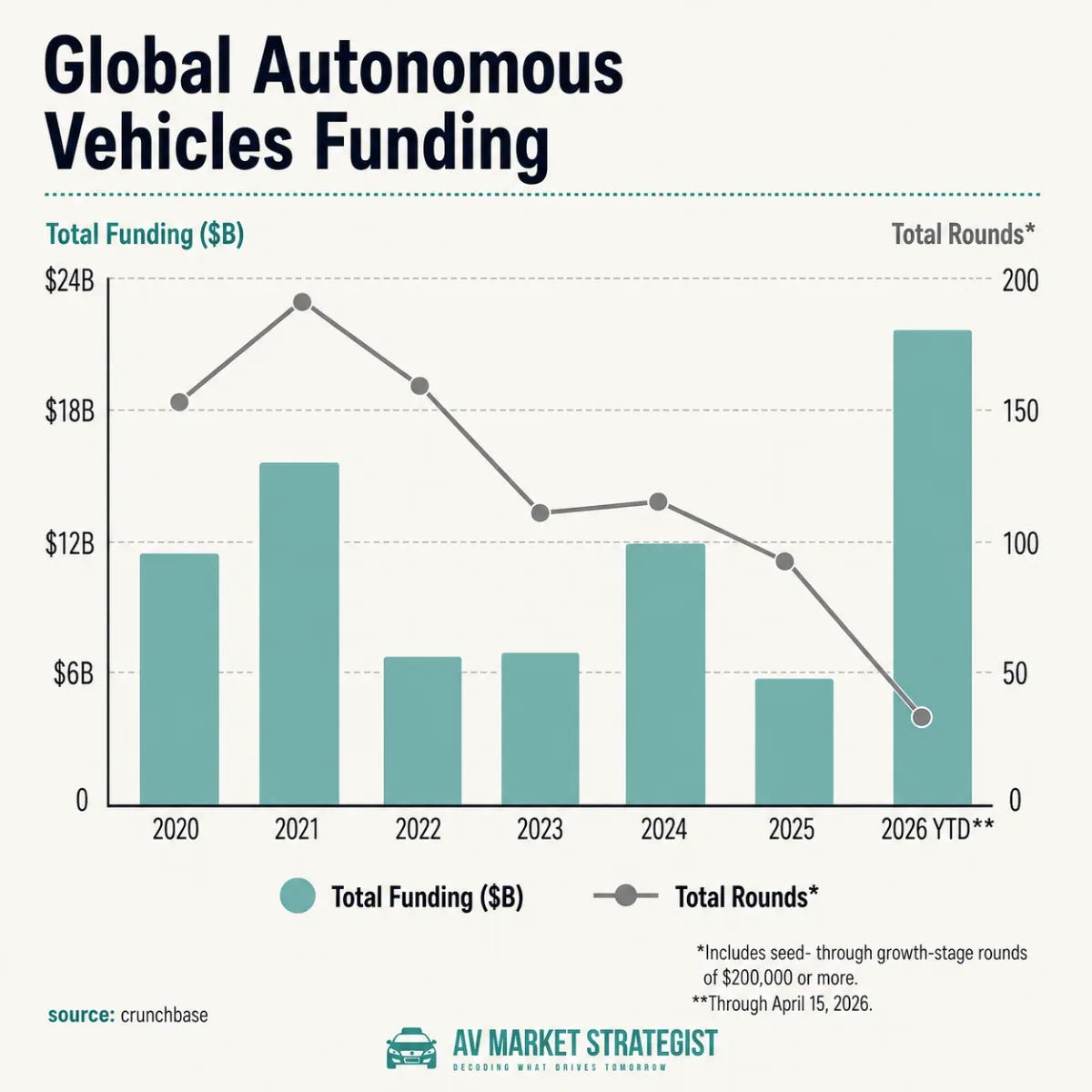

Autonomous driving is finally picking up real momentum, and the capital flooding into the sector is the clearest proof. Autonomous-vehicle startups raised a record $21.4 billion in the first months of 2026 alone, more than triple the $5.9 billion raised in all of 2025 and well above 2024’s $12.1 billion. The striking part is not the total. It is the concentration. The money tripled while the number of deals collapsed: just 34 deals so far in 2026, against 99 across all of 2025 and 127 in 2024.

Investors have stopped spreading small bets across dozens of startups and started pouring billions into the few players they believe will own the market.

And one company towers over even that concentrated field. Three-quarters of that $21.4 billion, $16 billion of it, went to a single name: Waymo, the autonomous driving subsidiary of Alphabet, Google’s parent company, raised at a $126 billion valuation. Read that again. One company absorbed roughly 75% of all the venture capital that flowed into the entire global autonomous-vehicle sector this year. The market has done more than pick favorites. It has crowned a leader. Waymo runs more than 500,000 paid driverless rides a week across 11 metros, and no one else in the West is close.

If you follow AI, here is why Waymo belongs on your radar specifically. Autonomous driving is the first large-scale, real-world application of physical AI. Most of what we call AI still lives on a screen, generating text, images, and code. Waymo is AI operating in the physical world, at scale, every single day. If you want to know what embodied AI looks like once it leaves the demo and meets the open world, this is the closest thing we have to a finished example. That is what makes it worth your time.

There are two ways to read Waymo in 2026. Read one way, it is the most successful deployment of physical AI on the planet, the company that turned a research project into 500,000 paid driverless rides a week and a $126 billion valuation. Read another way, it is a company whose technical lead is real but whose growth is now gated by things software cannot fix on its own: factory capacity, fleet financing, regulators, and the politics of where its cheapest cars are built. Both reads are true. This piece is about holding them at the same time.

There is one more thread worth flagging up front, because it runs through everything below. That same Crunchbase data shows the fastest growth in deployment, and several of the largest non-Waymo rounds, coming out of China. That is the tell. Winning the technology was step one, and Waymo won it. Step two is building, financing, and deploying fleets at cost, and on that measure the competition that should worry Waymo is not where most Western coverage is looking. It is in China. We will get there.

Let me show you the whole picture.

Where Waymo came from

A little background before we get into the numbers, because the origin explains the position.

Waymo began in 2009 as Google’s self-driving car project, an internal moonshot (nicknamed Project Chauffeur) built around the engineers who had won the US government’s DARPA autonomous-driving challenges a few years earlier. For most of the following decade it was a research effort, quietly logging test miles while the rest of the industry kept insisting the technology was perpetually five years away. In 2016, Google spun it out as a standalone company, Waymo, under the newly created Alphabet holding structure. In 2018 it launched Waymo One, its commercial robotaxi service, in the suburbs of Phoenix, and opened that service to the general public in 2020. Everything since has been the slow, expensive work of turning a science project into a business.

That lineage matters for two reasons that run through this entire piece. First, Waymo has been at this longer than anyone else still standing, which is why its safety and mileage record dwarfs every competitor’s and why its Driver generalizes to new cities the way it now does. Second, and less obvious, it sits inside Alphabet. That gives it access to Google’s compute, to DeepMind’s AI research, and to a parent patient and rich enough to absorb a decade of losses and bankroll a capital-heavy fleet. It also means Waymo never had to go public to survive

One frame to carry into the rest of this piece: because Waymo’s Driver has to operate in the open physical world rather than on a screen, the things that constrain it now are physical, not algorithmic. Factories, fleets, charging depots, regulators. That is why this market moves at the speed of manufacturing and policy rather than the speed of software, and it is the single most important thing to understand about why the leader is simultaneously far ahead and strangely stuck.

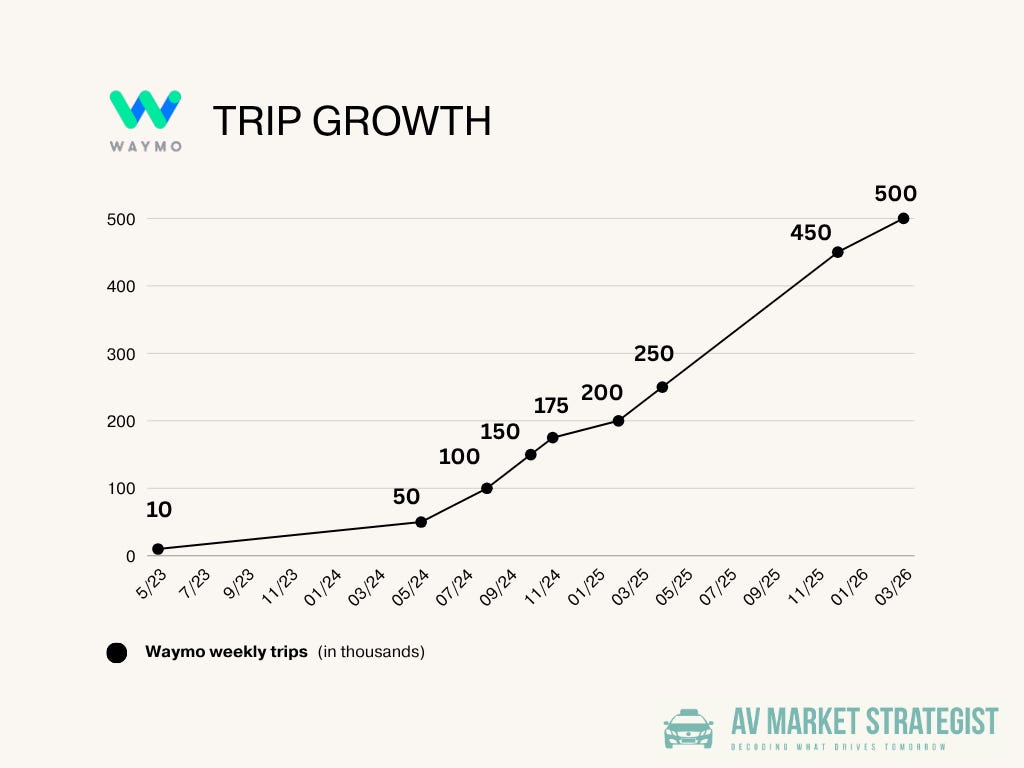

The growth curve: a 50x run in three years

Waymo’s ride volume is the cleanest evidence that the technology question is settled. The trajectory:

-

May 2023: 10,000 paid rides per week

-

May 2024: 50,000 per week

-

August 2024: 100,000 per week

-

October 2024: 150,000 per week

-

February 2025: 200,000 per week

-

April 2025: 250,000 per week

-

December 2025: 450,000 per week

-

March 2026: more than 500,000 per week

That is a 50x increase in under three years, and the curve steepened in the back half rather than flattening. Co-CEO Tekedra Mawakana has said the company is on track to pass 1 million trips per week by the end of 2026. Cumulative paid rides crossed 20 million by December 2025. On the safety side, the Waymo Driver had logged more than 170 million fully autonomous miles through the end of 2025, and passed 200 million in February 2026.

Two numbers turn this from a vanity metric into a thesis.

The first is the safety record those miles produced. In its March 2026 update, Waymo reported that across 170 million driverless miles, the Driver was involved in roughly 13 times fewer serious-injury-or-worse crashes than human drivers over the same roads, with 82% fewer injury-causing crashes and 92% fewer pedestrian-injury crashes. You can argue with the methodology at the margins, and people do. You cannot argue that the system is unsafe relative to the human baseline. The data is not close.

Source: Waymo Safety Hub

The second is what the curve says about the underlying model. For years, the knock on Waymo was that it only worked because it had memorized a few cities with painstaking high-definition maps, the “crutch” Elon Musk spent years deriding. That story is now hard to defend. Waymo compressed its city launch timeline from years (Phoenix and San Francisco each took the better part of a decade from first testing) to months: Dallas went from manual mapping to driverless testing in about four months, Houston in about six. In one week in December 2025, the company added four cities at once. In a single day in early 2026, it went from six commercial cities to ten. That is not what a company looks like when it is hand-crafting each deployment. That is a generalizable driver going to work.

The “Waymo works but can’t scale” narrative is dead, and it died on the ride curve, not in a press release. The question the curve cannot answer is whether 1 million rides a week is reachable on the current fleet, because, as we will see, the binding constraint moved from software to steel. Watch whether weekly rides keep their slope through 2026 or bend.

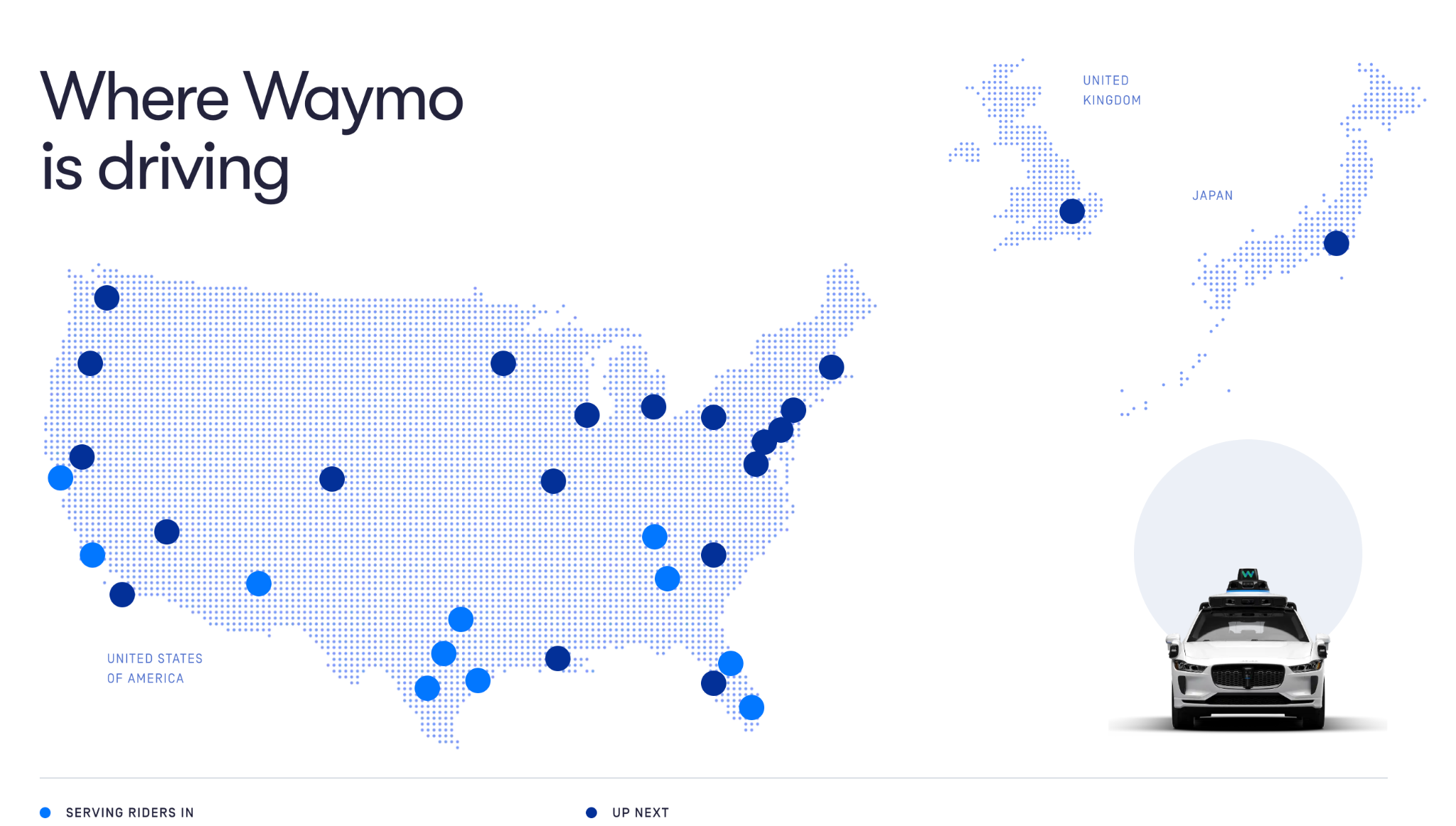

City evolution: from one metro to a national map

The ride curve is a function of the map, so look at the map.

As of mid-2026, Waymo offers paid driverless rides in 11 major metros, with a cumulative operating area that crossed 1,400 square miles after a single 27% expansion wave. The footprint:

Three things in that table tell the strategic story.

First, the way you hail a Waymo is different in almost every city, and that is deliberate. In San Francisco and Los Angeles, Waymo operates solo through its own app. In Phoenix, it runs a hybrid, available both in its own app and through Uber. In Austin and Atlanta, you can only get a Waymo through the Uber app. In Nashville, it is the Waymo app first, with Lyft integration to follow. This is a company running controlled experiments on who controls the customer. Hold that thought, because it is the heart of the Uber section.

Second, the fleet operations partner changes city by city too: Moove here, Avis there, Avomo for the Uber markets, Lyft’s Flexdrive in Nashville. The demand partners get the attention, but underneath them Waymo is running a parallel experiment on who actually owns and services the cars. That is the second layer of the partner stack, and it is where the unit economics live.

Third, look at the launch dates. Eight of the eleven metros opened in roughly 15 months. The map is not filling in linearly. It is accelerating.

And the announced pipeline dwarfs the live map. Waymo has started mapping or testing in Chicago, Charlotte, Sacramento, Boston, Baltimore, Pittsburgh, St. Louis, Minneapolis, Tampa, New Orleans, Detroit, Las Vegas, San Diego, Denver, Seattle, and Washington, D.C. Several of these matter beyond the dot on the map. Chicago, Denver, and Boston are cold-weather, snow-belt cities, and snow has long been the “Waymo only works in the sunbelt” rebuttal. Putting the Driver into Denver, the company’s coldest market to date, is a direct answer to that.

Internationally, Waymo is testing in London (around 100 Jaguar I-Paces across 100 square miles since April 2026, with Moove handling operations) and has begun data collection in Tokyo, its first introduction to roads outside the United States. Both are early. Both are strategically loud, because they are dense, high-value markets where a robotaxi has to handle genuinely harder driving than suburban Phoenix.

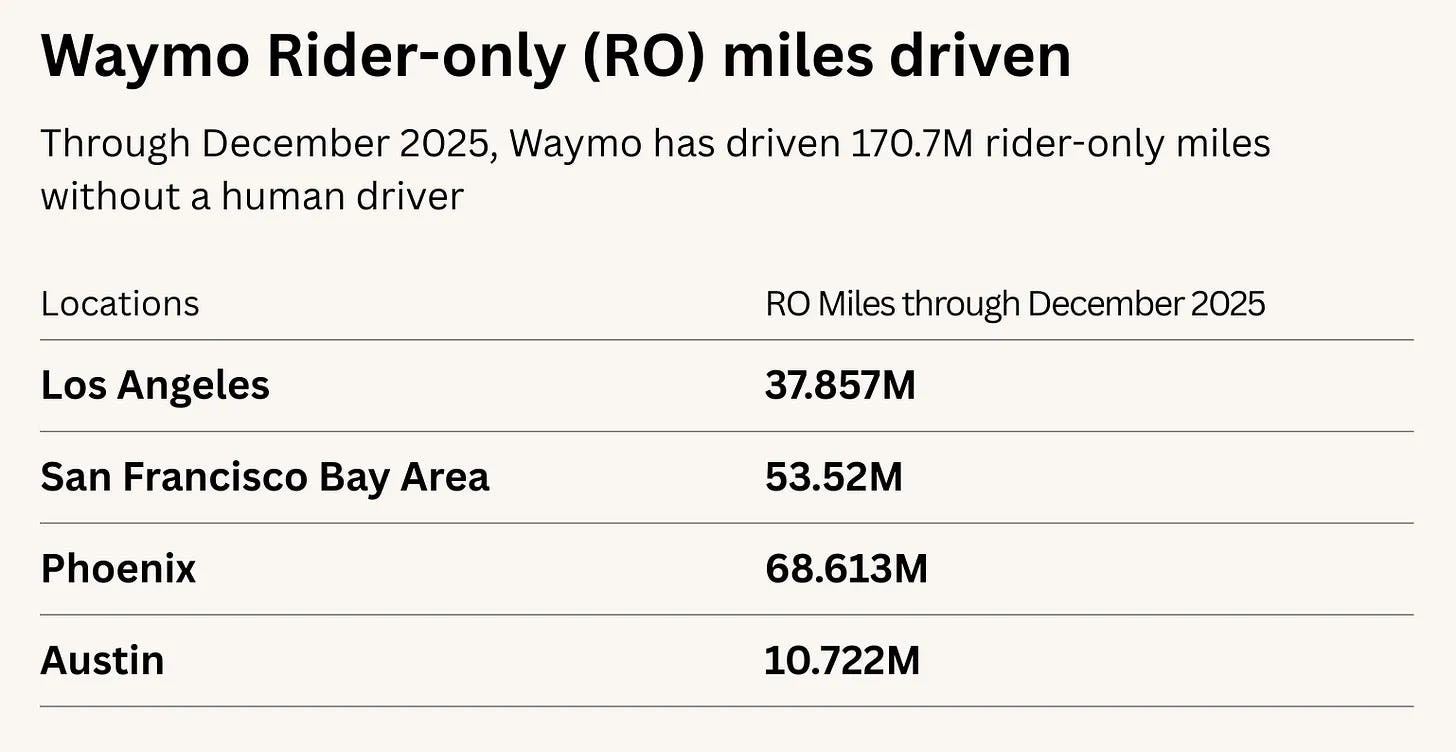

There is one detail inside the growth that deserves a flag. Using Waymo’s own rider-only mileage data, which get updated quarterly, the distribution across cities is shifting in a revealing way.

Phoenix, long the anchor, is declining as a share of total miles every quarter (around 40% of rider-only miles in Q4 2025, down steadily). Los Angeles is gaining share consistently. San Francisco is roughly flat, the profile of a mature market. Austin is ramping off a small base.

Read optimistically, this is exactly what healthy expansion looks like, with growth migrating to newer markets. Read more carefully, the deceleration in California’s incremental rides (more on this later) suggests the newer markets are absorbing fleet that the mature ones could otherwise have used. The map is growing. The cars to fill it are the question.

The generalizable driver turned city expansion from a multi-year engineering project into something closer to a rollout. The constraint is no longer “can the Driver handle Nashville.” It is “how many cars can we put in Nashville, and who owns them.” Watch the cold-weather launches (Denver, Chicago, Boston) and London. If those convert from testing to paid service on schedule, the last “it only works in easy conditions” argument is gone for good.

Under the hood: the Driver became a foundation-model problem

It is worth a short detour on why the city launches compressed from years to months, because the answer is the same shift that has reshaped the rest of AI.

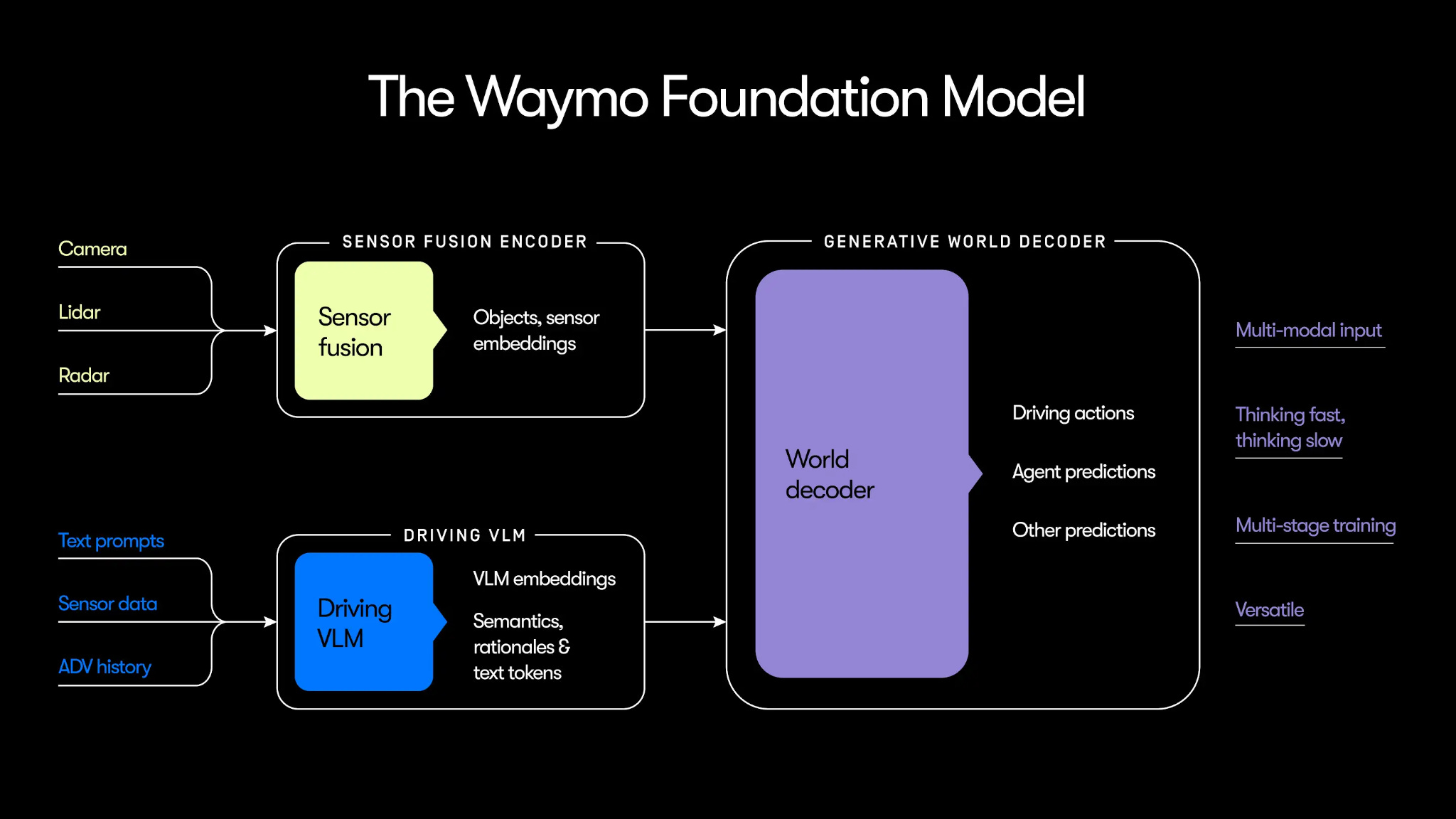

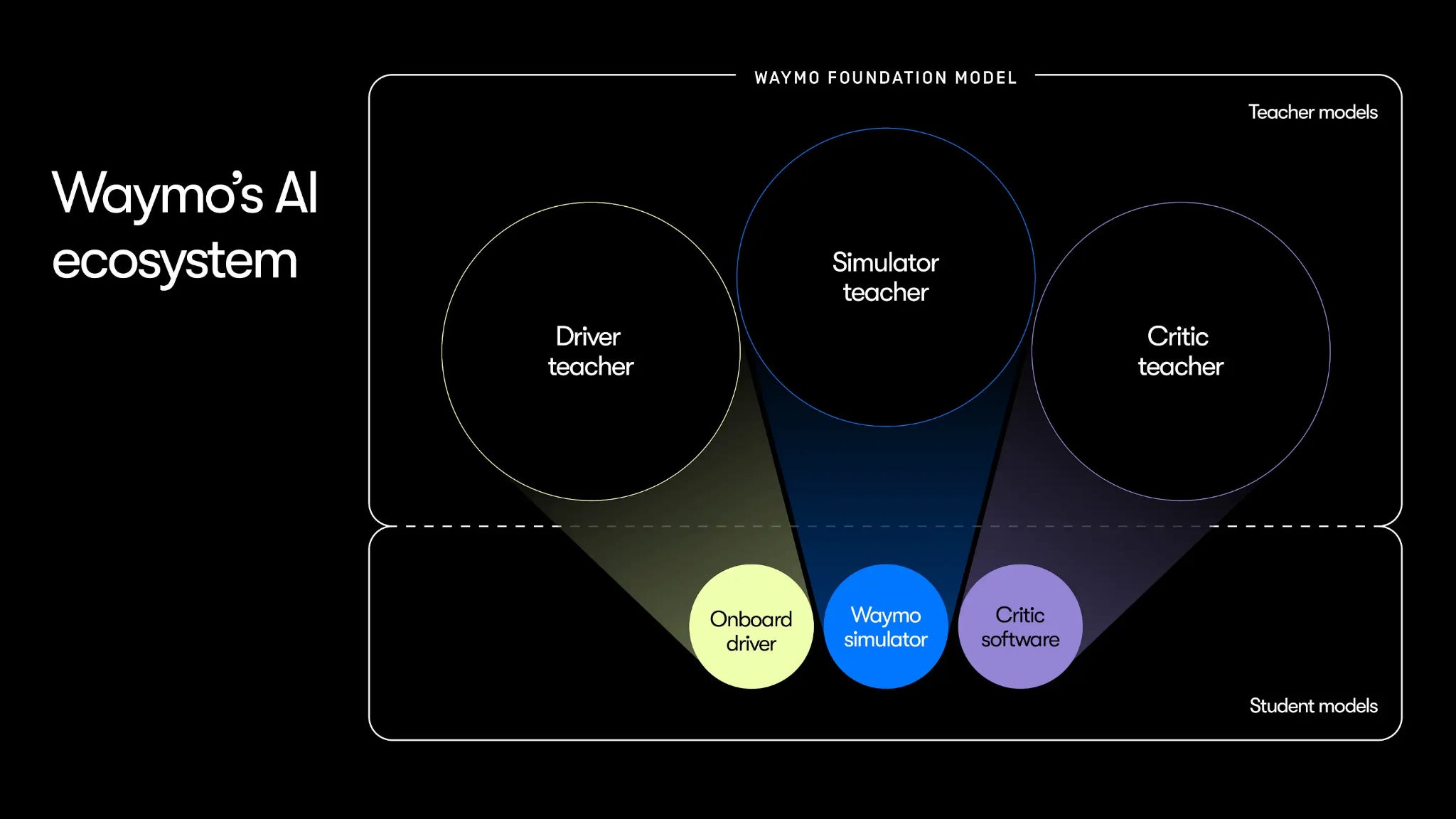

For most of its history, Waymo’s Driver leaned heavily on hand-built, high-definition maps and a modular stack of separately engineered components for perception, prediction, and planning. That is the approach Elon Musk spent years mocking as a dead end that could never generalize. The criticism had a kernel of truth a few years ago. It does not hold today, because Waymo’s architecture moved.

The current Driver is built around what Waymo calls a Foundation Model, and it is a hybrid rather than the pure end-to-end neural network that some rivals chase.

The shape of it: a very large, Gemini-derived “teacher” model, trained on Alphabet’s compute, distills its capability into smaller, faster in-vehicle “student” models, the vision-language models (VLMs) that actually run on the car in real time. The teacher knows a great deal; the student is small enough to make split-second decisions on the road. That teacher-student structure is why a new city no longer requires bespoke engineering. The model generalizes, and the maps become a prior rather than a crutch.

Alphabet-specific advantages compound here, and they are the part rivals genuinely cannot copy. Simulation. DeepMind’s Genie line of world models lets Waymo train and stress-test the Driver in vast synthetic environments, generating rare and dangerous scenarios on demand rather than waiting to encounter them on real roads. For a system whose hardest problem is the long tail of weird situations, the ability to manufacture the long tail in simulation is a structural edge.

Source: Waymo

Waymo has also started turning its model into a public yardstick. Its Reference Driver benchmark, published with TU Delft and built on an “active inference” framing, is an attempt to define what a safe driver should do and measure against it. I read that as transparency deployed as a competitive weapon: if Waymo sets the benchmark, every rival gets graded on Waymo’s terms. The honest caveat is that Waymo is, in part, grading its own homework.

The technical moat is no longer “we mapped this city.” It is “we have Alphabet’s compute, Gemini, and DeepMind’s simulation behind the Driver.”

Fleet growth and the binding constraint: vehicle supply

Here is the pivot in the whole story.

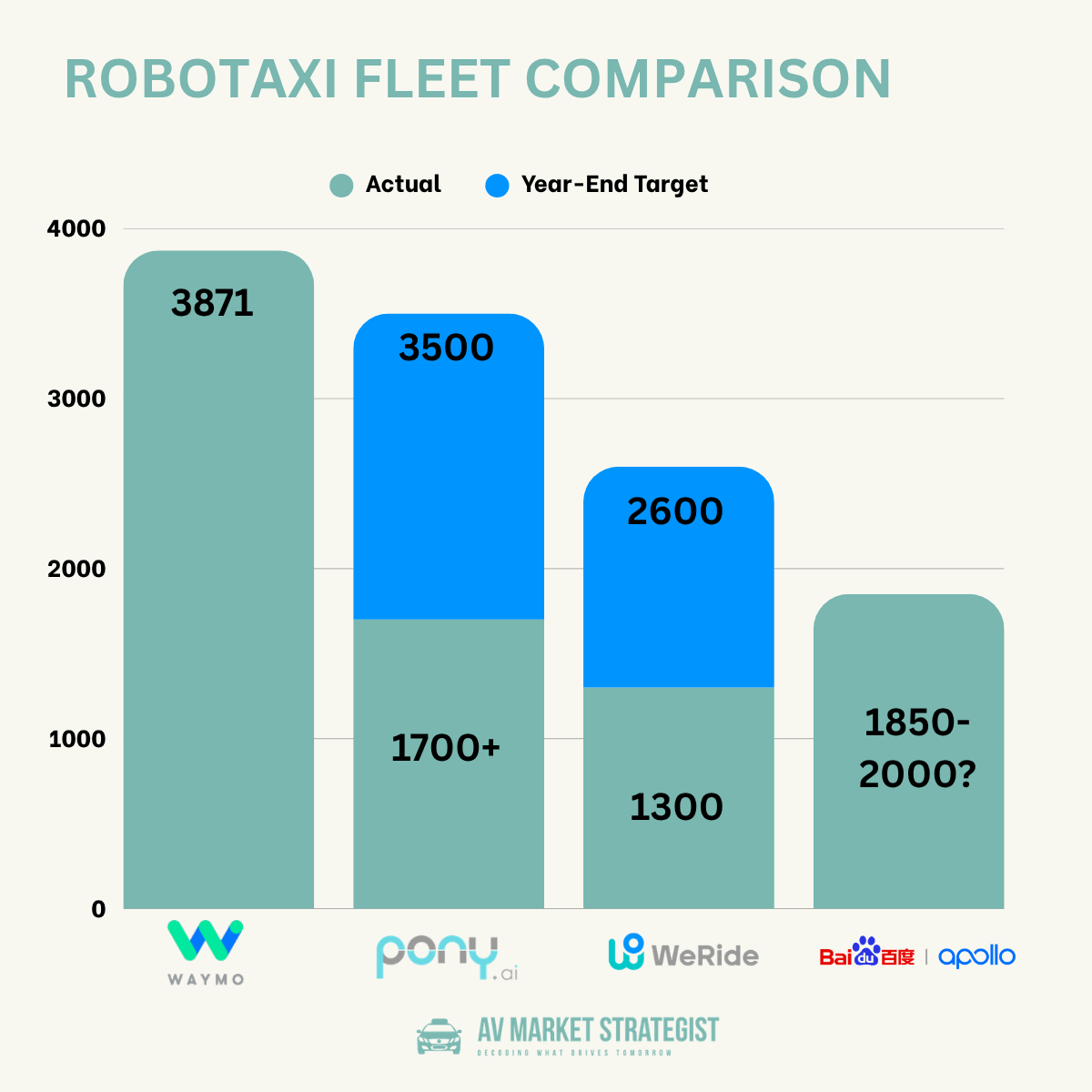

Waymo’s fleet grew from about 2,500 vehicles in late 2025 to a stated 3,000 in February 2026. The more reliable read comes from its recall filings with NHTSA, the US auto-safety regulator: a flooding recall covered 3,791 vehicles, and a June 2026 freeway recall covered 3,871, described as effectively the entire US fifth-generation fleet. So the real number is closer to 3,900 than to “around 3,000.” Call it roughly 3,900 cars running more than 500,000 rides a week across 1,400 square miles.

Now set that against the ambition. To reach 1 million rides a week and to fill a pipeline of more than a dozen new metros, Waymo needs to go from thousands of vehicles to tens of thousands. The Driver can already handle those cities. The company simply does not have enough cars. This is the single most important sentence in any honest Waymo analysis: the company solved the technology and is now supply-constrained on vehicles.

That reframes everything Waymo has done over the past 18 months. The flurry of deals that look like a procurement story are actually the entire growth strategy. Waymo is building a multi-pronged manufacturing stack:

-

The Jaguar I-PACE, the current workhorse, is being wound down as the primary platform. It is expensive (roughly $75,000 for the base vehicle + Sensor costs). At that cost, scaling to tens of thousands is brutal.

-

The Zeekr platform, internally the basis for Waymo’s first purpose-built robotaxi (the “Ojai”), is the cost answer. It is designed in Sweden, built by Geely’s Zeekr in China, and finished in Arizona. Analysts peg Zeekr’s base vehicle cost near $38,000, a meaningful step down. It is also, as we will see, a political liability in red states, precisely because it is built in China.

-

The Hyundai Ioniq 5 is the volume answer in the US. Waymo and Hyundai have a confirmed partnership to build Ioniq 5 robotaxis at Hyundai’s Metaplant in Georgia. The headline specifics that get quoted, up to 50,000 vehicles by 2028 and a deal worth roughly $2.5 billion, trace to reporting (notably the outlet Gasgoo) rather than a full Waymo disclosure, so I would treat the exact figure as reported, not confirmed. The reasonable inference is on the method: at that kind of volume, the autonomy hardware almost has to be integrated on the production line rather than retrofitted car by car, and that line-fit approach is the difference between a factory and a workshop. The integration method itself is my read, not a published spec.

-

The Phoenix upfit facility, where Waymo integrates the Driver, is scaling toward “tens of thousands of vehicles per year.”

-

And in a move that is half capacity and half symbolism, Waymo bought Apple’s old 5,500-acre vehicle proving ground for around $220 million, the former testing site for Apple’s abandoned car project. Waymo now validates new platforms on the field Apple walked away from.

This suggests the “tens of thousands per year” upfit capacity referenced in Waymo’s blog post could be largely additive to the Hyundai volume. Phoenix handles Zeekr vehicles that can’t be integrated in China. Georgia handles Hyundai vehicles with line-fit installation. So this could push the supply to 60,000-70,000 vehicles by 2028 when both pipelines are fully operational.

I want to be clear that this is my interpretation of stated capacity, not a number Waymo has guaranteed, and supply plans slip. But the direction is unambiguous: Waymo is trying to turn itself into a company that can put out robotaxis at automotive scale, because that, not the Driver, is now the bottleneck.

This is also the right place to introduce the comparison that runs through the rest of this piece. People benchmark Waymo against Tesla and Zoox because those are the famous American names. The fleet numbers say that is the wrong benchmark.

Tesla’s unsupervised robotaxi fleet in Austin sits at roughly 20 to 25 vehicles and has been contracting even as it expands its map, because a geofence is free and cars are not. Zoox, backed by Amazon and genuinely impressive on the product, is still measured in the low hundreds, with a stated facility capacity of up to 10,000 vehicles a year that it has not yet filled. Meanwhile Pony.ai is targeting more than 3,500 robotaxis in 2026, WeRide runs around 1,300 robotaxis inside a total fleet near 2,800, and Baidu’s Apollo Go is doing 300,000-plus rides a week at peak across 26 Chinese cities. The companies operating in Waymo’s weight class are, overwhelmingly, Chinese. We will come back to why that matters more than anything Tesla announces.

Vehicle platforms and the cost curve: why Waymo bought a Chinese car

The platform shift deserves its own beat, because it is where Waymo’s strategy collides with geopolitics.

The economic problem is straightforward. We have no official data on the cost of the Jaguar I-Pace robtaxis, but at an estimated $150,000 to $175,000 per Jaguar, a 60,000-vehicle fleet runs to roughly $9 billion to $10 billion in hardware alone. Every dollar shaved off the per-vehicle cost compounds across tens of thousands of cars and directly determines when, and whether, the unit economics of a robotaxi ride beat a human-driven one. So Waymo is doing two things at once: dropping to cheaper base vehicles, and cutting the cost of its own sensor-and-compute kit.

On the kit, the sixth-generation Waymo Driver is the lever. It moves to higher-resolution cameras (17 megapixels) while cutting the camera count from 29 to 16, is built to run on multiple vehicle platforms, and is engineered for winter conditions. Fewer, better sensors mean a cheaper, more manufacturable system. The sixth-gen Driver is, in the company’s framing, the engine for the next era, and the reason it can spread across Jaguar, Zeekr, and Hyundai bodies rather than being bespoke to one.

On the vehicle, the math pushed Waymo toward China, and that is the uncomfortable part. The cheapest, most production-ready purpose-built robotaxi body available to Waymo came from Geely’s Zeekr. So Waymo’s answer to its single biggest constraint, cost, was to source a Chinese-built vehicle, design it in Sweden, and finish it in Arizona. Under Chinese export rules, the cars ship as “shells” stripped of certain connectivity, with the intelligence added stateside. It is an elegant supply-chain solution and a political grenade. In a US environment where Chinese-built vehicles are increasingly treated as a national-security question, putting thousands of China-made robotaxis on American streets, especially in red states like Texas, is a liability that has nothing to do with how well the car drives.

That is exactly why the Hyundai Ioniq 5 deal matters beyond its volume. It gives Waymo a politically clean, US-built platform to lean on, which is why the likely outcome is a bifurcation: the Zeekr platform abroad and in friendly markets, the Hyundai for the bulk of US expansion.

The partner stack: demand on one side, fleet on the other

To understand Waymo’s business, separate its partners into two layers, because they do completely different jobs.

The first layer is demand: who brings riders and who owns the customer relationship. This is where Uber and Lyft sit, alongside Waymo’s own app, Waymo One. Waymo’s pattern here is deliberate experimentation, as the city table showed. Solo in San Francisco and Los Angeles. Hybrid in Phoenix. Uber-exclusive in Austin and Atlanta. Lyft-integrated in Nashville. In June 2026 Waymo also launched Waymo Premier, a $30-per-month subscription offering priority pickups, 10% cash back, early access, and free cancellations. That is more interesting than it looks. Waymo cannot summon more drivers at peak the way Uber can, because it owns its fleet. A subscription is one of the few levers it has to manage demand and build recurring, higher-margin revenue on top of a fixed supply of cars.

The second layer is fleet operations: who actually buys the cars, parks them, charges them, cleans them, and maintains them. This is the unglamorous, capital-heavy work that determines whether a robotaxi ride makes money, and Waymo has been steadily handing it off:

-

Moove, a Nigerian-founded, Uber-backed fleet operator, runs Waymo’s operations in Phoenix and Miami and is the operator for London. Moove raised a $1.2 billion oversubscribed debt round specifically to buy and operate vehicles for Waymo. The fact that debt investors oversubscribed a round to own depreciating robotaxis is itself a signal: the market now believes AV cash flows are predictable enough to lend against.

-

Avis Budget Group is the end-to-end fleet partner in Dallas, handling infrastructure, vehicle readiness, maintenance, and depot management. Avis brings a 180-country network and pre-built EV charging infrastructure, which addresses one of the least-discussed bottlenecks in this business: energy. A robotaxi that cannot charge is a robotaxi that is not earning.

-

Avomo (formerly Moove Cars, and a distinct entity from Moove.io) runs fleet management for the Uber-operated Waymo service in Austin and Atlanta. The distinction matters: in the Uber-exclusive cities, the fleet operations sit under Uber’s partner, not Waymo’s.

-

Lyft’s Flexdrive subsidiary handles fleet operations in Nashville. Flexdrive owns and operates around 15,000 vehicles, and Lyft argues that owning the operational stack lets it extend the AV cost advantage to 25%, by keeping the operator margin in-house rather than leaking it to a third party.

-

Element Fleet Management, the world’s largest publicly traded automotive fleet manager, signed a multi-year deal with Waymo in June 2026, starting with end-to-end operations in San Diego, a new Waymo market, with more cities to follow. Element is a different species from the AV-native operators: roughly 1.56 million vehicles under management, about $1.2 billion in 2025 net revenue, a 56% adjusted operating margin, Blackstone-backed funding, and a market cap near $8 billion. It brings three things startups cannot: scale, public-market discipline, and an institutional capital base. Its data systems alone identified $1.6 billion in client cost savings last year.

-

Transdev, the operator almost nobody writes about, has quietly been running Waymo’s fleets the longest. The French multi-modal transit giant (around 12.8 million passengers a day across buses, trains, trams, and ferries) has handled Waymo depots, maintenance, charging, and remote supervision through its TAS subsidiary since 2019, before most of the names above existed in this business. More than a thousand of its people already do this work across Phoenix, San Francisco, Los Angeles, and Austin.

That is now a six-way race for a job that barely existed eighteen months ago: Moove, Avis, Avomo, Lyft’s Flexdrive, Element, and the long-running Transdev. The reason so many large, serious companies are crowding in is that the operating layer is becoming an industry of its own. One analysis pegs the AV fleet-operations market at $12.8 billion by 2034. The cleanest analogy is aviation, where the durable money sits less with the airlines than with the ground handlers who fuel, clean, and turn the aircraft around between flights. These companies are positioning to be the ground handlers of autonomy, and Waymo’s willingness to rent the entire layer rather than build it is the clearest sign yet that this is a real, separable business.

The partner stack is where Waymo decides what kind of company it wants to be: a vertically integrated operator carrying cars on its own balance sheet, or an asset-light licensor of the Driver. The evidence points toward the licensor model, slowly. This would also fit Alphabet’s DNA. Watch whether Waymo starts pushing vehicles off its balance sheet onto Moove, Avis, and others.

The Uber relationship: from strategic alliance to transaction

If you want to understand where Waymo is going, watch what it is doing to Uber.

For a while, the Waymo-Uber relationship looked like an alliance: Waymo, the only company in the United States offering paid driverless rides at meaningful scale, paired with Uber, the platform with the demand. The flagship of that alliance is “Waymo on Uber,” live in Austin and Atlanta, where the only way to hail a Waymo is through the Uber app. Request an UberX or Uber Comfort, opt into Waymo, and if one is available you might be matched to a driverless car.

That arrangement is now better described as transactional than strategic. And transactional relationships have shorter expiration dates than alliances do. The evidence has been accumulating for over a year:

-

Since launching Waymo on Uber in Austin and Atlanta, Waymo has announced close to a dozen new markets, and none of them included Uber. Every solo launch is a quiet statement that Waymo does not need Uber to grow.

-

In Nashville, Waymo partnered with Lyft, Uber’s primary rival. That is not a neutral act.

-

Uber’s own executives started taking public shots, including a chief technology officer posting criticism of Waymo, the kind of thing professional C-suites at this level almost never do in public. Whether it was a deliberate message or a slip, it signaled that the partnership had gone rocky.

-

Uber published a lengthy AV policy white paper making the case for cities and for platforms, widely read as a case against the single-operator robotaxi model, which in the US means Waymo. The two companies have since been trading jabs in the press, including a fight over whether Waymo deliberately avoids lower-income neighborhoods like Oakland (Waymo’s constraint there is partly that it has not been permitted, not that it refuses to serve).

The structural reason underneath all of it is the customer. In San Francisco and Los Angeles, Waymo and Uber are direct competitors, not partners. There is no friendship in those two markets. And the design of Waymo on Uber reveals the tension: there is no dedicated “autonomous only” tier in the Uber app in the US. You cannot open Uber and demand a Waymo. My read on why is that a dedicated AV tier’s branding and leverage risk scales with how concentrated the market is. In the US, a dedicated AV tier would effectively be a Waymo tier, and the moment riders learn they can summon a Waymo, many of them stop thinking of it as an Uber at all and start downloading the Waymo app. Uber cannot afford to teach its own users to leave.

So who loses if this breaks fully? In the short term, clearly Uber. Roughly 99% of Uber’s business is still human ride-hail, but its investors do not price the 99%, they price the AV question. By one count, around 70% of the questions on recent Uber earnings calls were about autonomy. Waymo is the only company offering paid driverless rides at scale in the US, which means Waymo is the only partner that “counts” for Uber’s AV narrative right now. Losing exclusive access to it, or watching it cozy up to Lyft, hits Uber where investors are looking.

Uber’s response tells you it understands the exposure. It is executing a deliberate fragmentation strategy: invest in and partner with as many AV players as possible so that no single one, read Waymo, gains pricing power over the platform. Uber has put money into Nuro (a total commitment around $500 million), Waabi, Lucid, Avride, WeRide, and Wayve (which will power Uber’s London fleet), and an Autobrains program in Munich. It is building Uber Autonomous Solutions (insurance, mission control, fleet financing, mapping), Uber AV Labs (a 500-vehicle, sensor-equipped data fleet logging around 2 million miles a month to serve partners), and, for the first time in its history, it is agreeing to buy vehicles outright from partners like Lucid. A company that scaled to millions of rides a day without ever owning a car is now buying cars. That is how existential Uber considers this.

Here is the two-lens read, and where I will give you my actual position. Read one way, the breakup is already happening and it is bad for Uber: Waymo is disintermediating the largest demand aggregator in the West, proving it can grow without it, and steering its most valuable customers into its own higher-margin app. Read the other way, this is a short-term divorce that reconciles long-term, because Uber genuinely solves a problem Waymo has, peak-demand utilization, and a fixed fleet that cannot flex up on a Saturday night will eventually want access to Uber’s overflow demand. I lean toward the first read for the next year or two: the direction of travel is separation, and the data points are too consistent to call it noise. But I hold it loosely, because the binding constraint here is utilization economics, not animosity, and utilization math has a way of pushing rivals back into the same bed. The honest answer on the long term is that we do not know yet, though the near-term trajectory clearly points to “transactional and cooling.”

The costs of being the leader: every 10x breaks something new

Now the counterweight, because a deep dive that only catalogs the wins is marketing, not analysis.

Waymo’s recurring problem is the most enviable kind: every time it scales by an order of magnitude, it surfaces a new class of failure that smaller operators never hit. The list as of mid-2026:

-

The San Francisco blackout. During a power and connectivity disruption, roughly 1,593 Waymo vehicles paused at once, a confirmation-protocol overload where too many cars asked for human guidance simultaneously. It was not a crash. It was a coordination failure that only exists at fleet scale.

-

The school-bus probe. NHTSA opened an investigation after Waymo vehicles repeatedly failed to handle a stopped school bus correctly, with 19 instances in Austin that persisted even after a software update. School buses are a bright-line safety issue, and “we patched it but it kept happening” is the kind of sentence regulators remember.

-

The flooding recall. The 3,791-vehicle recall came after an empty robotaxi was swept into a San Antonio creek, and the reporting suggested the fixes were “not sticking” cleanly. Weather edge cases scale with geography, and Waymo’s geography is expanding fast.

-

The freeway recall. In June 2026 Waymo filed a recall covering 3,871 vehicles, effectively its entire US fifth-generation fleet, after a documented pattern of cars driving at speed into freeway construction zones (two Phoenix incidents in April, seven Bay Area vehicles driving between cones into a closed lane in May). With no software fix ready, the interim remedy was blunt: every vehicle restricted from freeways. This is the fourth recall in roughly 28 months, and the fleet grew across the filings, which is its own quiet tell about scale. It stings more than a normal recall because freeway access is the capability that lets a robotaxi compete with an ordinary ride-hail trip. And the timing is the whole industry in miniature: Waymo hired a fleet manager to scale faster and pulled itself off the freeway in the same week. Read one way, recalling proactively with no fix in hand is exactly how a safety-led operator should behave. Read another way, the operating layer just reminded the leader how fragile scale is. Both are true.

My consistent read on all of this: these are the frictions of being big enough to matter, not evidence that the model is broken. Every one of these failure classes is a function of scale, and scale is exactly what Waymo’s competitors do not yet have to worry about. But there is a real risk hiding in the list, and it is not any single incident. It is transparency. Waymo’s safety lead is currently also a transparency lead, and transparency is regulatory currency. The moment Waymo drifts toward guardedness, redacting, minimizing, treating its data as a trade secret, it forfeits the very thing that earns it regulatory goodwill. The companies that share data openly will keep earning the benefit of the doubt. The ones that hide behind confidentiality will face growing skepticism.

The real race: why Waymo’s competition is in China, not Austin

Everything above leads to the conclusion that most Western coverage misses, so let me state it plainly. The race is no longer just about who drives best. It is about who can build, finance, and deploy fleets at cost, and prove it. And on that axis, Waymo’s serious competition is Chinese.

Look at who is actually scaling. Tesla, the perennial headline, has a shrinking unsupervised fleet of around 20 to 25 cars in Austin and logged zero autonomous test miles in California for a sixth straight year. The cleanest illustration sits in Texas, the state where Tesla builds its cars and enjoys every home advantage it could ask for: the first government-mandated fleet registry there counted 577 Waymo vehicles against 42 for Tesla. Its map grows; its fleet does not. Zoox has a beautiful purpose-built vehicle and Amazon’s balance sheet, but it is still in the low hundreds of vehicles. These are not the companies operating at Waymo’s order of magnitude.

The companies that are operating at that order of magnitude are Pony.ai, WeRide, and Baidu’s Apollo Go. Pony is targeting more than 3,500 robotaxis in 2026 and grew robotaxi revenue 395% year over year in Q1, and it is doing it across three vehicle platforms in parallel rather than one: the Toyota Bozhi 4X (the robotaxi version of the bZ4X, assembled on a GAC-Toyota line), the BAIC ARCFOX Alpha T5, and the second-generation GAC Aion V, all carrying its seventh-generation system, which cut the autonomy hardware bill of materials by 70% versus the prior generation. That multi-platform, OEM-assembled model is exactly the manufacturing setup Waymo is straining to reach, and Pony already has it running on production lines.

WeRide runs around 1,300 robotaxis with roughly a third of its fleet overseas, posted a group gross margin near 35% in Q1, and is expanding aggressively into Europe and the Middle East, where the economics are far better than at home. Overseas gross margins run close to 50%. WeRide’s Middle East subsidiary has already reached operational profitability on a standalone basis, according to CFO Jennifer Li on the Q4 2025 earnings call.

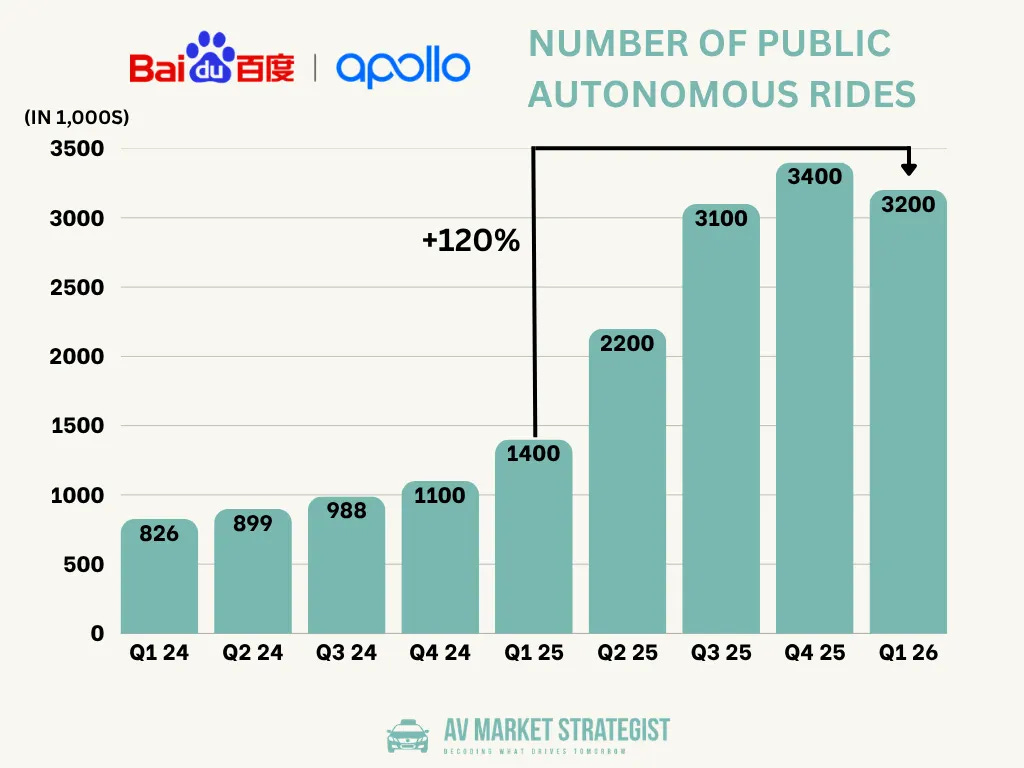

This explains why the Chinese players are racing into Europe & Middle East rather than digging in at home. Baidu’s Apollo Go is doing 300,000-plus rides a week at peak across 26 Chinese cities. These are not pilots. These are scaled operations with manufacturing behind them. In Q1 2026 Apollo Go delivered 3.2 million driverless rides.

And here is the thread that connects the whole piece. Chinese hardware controls the cost curve. It builds Waymo’s own Ojai robotaxi. It sits inside the supply chain of nearly every Western player. It funds the expansion of Pony, WeRide and Baidu Apollo Go. Waymo’s three fastest-scaling peers are Chinese, and Waymo’s own answer to its biggest constraint was to buy a Chinese-built car. When the binding constraint of an industry is manufacturing cost, the country that owns manufacturing cost owns the leverage.

The strategic implication for Waymo is uncomfortable but clear. Its technical lead is genuine and probably durable for a few years. Its scaling lead in the US is real. But the global race, in Europe, the Middle East, and Southeast Asia, is increasingly being run by an asset-light Chinese export machine that pairs local partners with Chinese tech and Chinese-cost hardware, and moves faster on regulatory entry than Western firms have shown they can.

The pace is the tell. In June 2026 alone, WeRide and Uber announced commercial robotaxi launches in Madrid and then Zurich, WeRide’s first two European markets, each run by a local operator and each following the same script: fare-charging late in 2026 with a safety driver, then the driver out by mid-2027, starting in premium markets where a still-expensive technology can clear breakeven first. That is the asset-light export machine in motion, and it is moving into Europe faster than Waymo is. Waymo is winning the US. The open question is whether winning the US is enough.

The bottom line

The bull case. Waymo solved the hardest problem in the industry, autonomous driving that is measurably safer than humans, and is the only Western company deploying it at scale. The valuation, rich as it is, is backed by Alphabet’s willingness to fund the capital intensity, by a multi-platform manufacturing strategy that bends the cost curve down, and by optionality (delivery, licensing, personal vehicles) that ride-hail revenue alone does not capture.

The bear case. The technology is no longer the constraint, and the new constraints are the ones Alphabet is least practiced at: manufacturing at automotive volume, financing a capital-heavy fleet, and navigating a regulatory and political environment that is fragmenting against it. The cheapest path to scale runs through a Chinese supply chain that is a political liability. Growth in mature markets is already decelerating on fleet constraints. And the global race is being set by Chinese players who own the cost curve.

What I’d watch into the rest of 2026.

First, vehicle supply. The Hyundai Georgia ramp and the Phoenix upfit capacity are the real story. If they hit, the rides curve holds. If they slip, everything slips with them.

Second, the Uber endgame. Watch whether Waymo ever launches another exclusive “Waymo on Uber” market. I doubt it will, and that absence is the tell that the alliance is functionally over.

Third, transparency. Waymo’s regulatory position is built on sharing its safety data. The day it starts hiding numbers is the day its strongest moat starts to erode. The companies that share data openly will keep earning the goodwill. The ones that hide behind confidentiality will face the skepticism.

And fourth, China. Not as a headline, but as the cost curve. The most important number in this industry is not Waymo’s ride count. It is the per-vehicle cost of a scaled robotaxi, and right now that number is being set in Shenzhen and Guangzhou, not Mountain View. Waymo has the best driver in the world. The race from here is about whether it can afford to put that driver in enough cars before someone cheaper catches up on everything else.

The technology question is closed. The manufacturing question is wide open. And that is the story of Waymo in 2026/2027.

Thanks for reading!

-

Before you go, please follow these AV Newsletters for more deep dives like this. For starters I recommend:

The AV Market Strategist

The Driverless Digest

Ottomate

Autonomous System Safety by Phil Koopman

Addendum and Future Considerations of Waymo

Is Waymo scaling successfully in 2026? I’d like to think so:

-

On the whole, Chinese cities are rolling out Robotaxis services faster than their peers in the United States, Europe or the Middle East. But China also has more active robotaxi players and a more complicated market.

-

Following its massive $16 billion funding round at a $126 billion valuation, the company is aggressively scaling its real-world network, targeting 1 million weekly paid rides by the end of the year.

-

Expansion and geographical marketshare: Waymo recently surged its coverage area to over 1,400 square miles across 11 major U.S. cities—a geographic footprint larger than the state of Rhode Island.

-

Waymo is expanding within its existing markets (like expanding across the SF Bay Area, Miami, Austin, and Atlanta). This drives up vehicle utilization rates and dramatically improves unit economics.

-

Customer loyalty is showing mixed signals in 2026: While Waymo’s core power users are intensely loyal, its overall user retention metrics still trail traditional ride-hailing heavyweights like Uber and Lyft.

-

The launch of “Waymo Premier” (a $29.99/month subscription program offering priority pickups and ride credits) proves that Waymo is successfully transitioning casual, novelty riders into a highly predictable, recurring revenue stream.

-

The TAM is so huge for robotaxis and frankly Waymo is in 2026 the clear leader in commercial robotaxis (autonomous ride-hailing) with proven technology, explosive real-world growth, improving unit economics, elite backing, and exposure to a transformative trillion-dollar mobility market.

-

Futurism tourists? Waymo’s lower average retention is heavily driven by its novelty. In highly concentrated markets like San Francisco and Los Angeles, a significant percentage of weekly downloads come from tourists, business travelers, or locals taking a single “novelty ride” to experience a driverless car, only to switch back to standard apps for daily transit.

-

The experience of Waymo’s system: Waymo operates the most advanced and widely deployed Level 4 autonomous system (“Waymo Driver,” now in its 6th generation). It uses a multi-sensor stack (LiDAR, radar, cameras) + HD maps + AI, trained on massive real-world data. As of March 2026, Waymo had driven 220.6 million rider-only autonomous miles. Not bad for a Google Spin-out Moon shot.

-

Major VCs and investors have joined the Waymo bandwagon. The latest funding round was led by Alphabet alongside previous backers, including Andreessen Horowitz, Fidelity, Perry Creek, Silver Lake, Tiger Global and T. Rowe Price. The new round includes additional investors such as Dragoneer Investment Group, DST Global, Sequoia Capital, Kleiner Perkins and Alphabet-owned investment firm GV.

I really like how Amazon’s Zoox looks too:

Let’s keep watching the future together.

“}]] Read More in AI Supremacy