Good Morning,

Today I actually want to talk about Datacenters, but there are some digital airwaves AI news to cover first. This is going to be a lot of curation and a lot of infographics but a measure of the State of AI as it is today, including AI Infra gridlock that seems to have a media ban. This kind of content takes me hours and hours to compile but is meant to be nibbled on. So bookmark it for weekend reading if it’s your style.

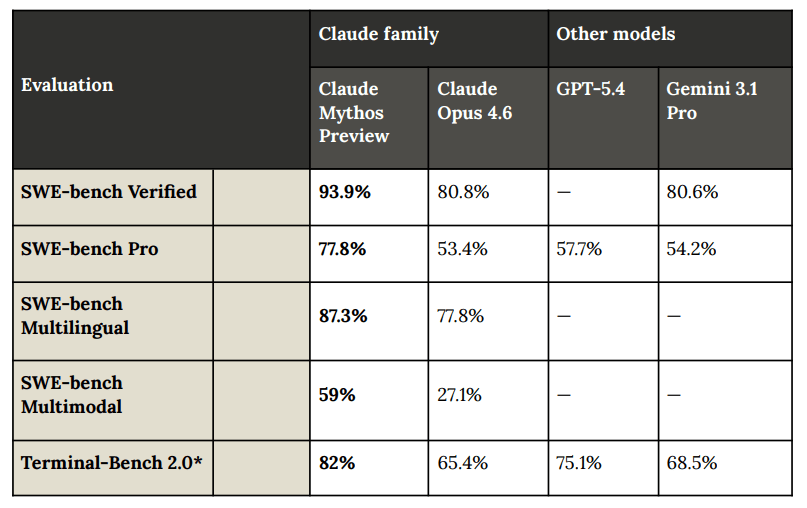

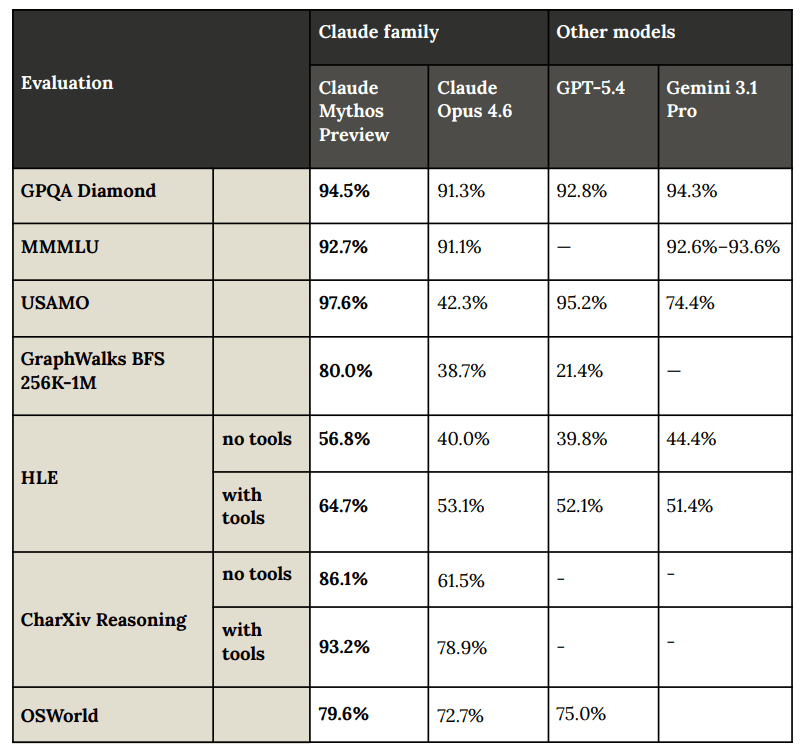

Anthropic’s latest model Mythos is getting a lot of scrutiny (okay fine, outlandish praise) as a massive “step-up” in model capability in coding and reasoning. We now leave behind the “Opus” family of models for Capybara models that are bigger and more capable. Anthropic released a Mythos System Card Preview that’s fairly interesting.

Mythos Models are so good they are Dangerous

Anthropic has developed a New Protocol for Releasing Models in a more Safe way: Project Glasswing

In essence, Anthropic’s new model, Claude Mythos, is so powerful that it is not releasing it to the public. Instead, it is starting a 40-company coalition, Project Glasswing, to allow cybersecurity defenders a head start in locking down critical software.

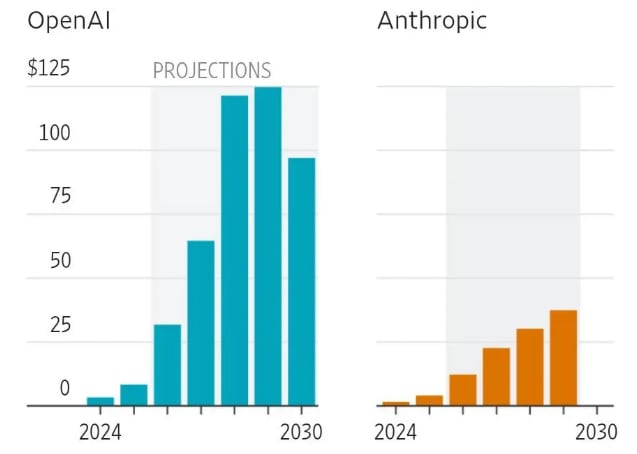

Anthropic’s Revenue (ARR) Surges in Early 2026

This as Anthropic’s ARR has hit $30 Bn. and is about to overtake that of OpenAI. The following are true stories:

-

Anthropic added the combined ARR of Palantir, Anduril, and Databricks—in one month. (via Lenny) – we had said 2026 would be a key year for Anthropic’s growth overtaking that of OpenAI.

-

Between February and April Anthropic went from $19B in February to $30B in March, 2026.

-

Anthropic’s revenue grew 30x in 15 months.

-

Said another way: They added $6B in ARR just in *February*. Companies like Palantir and Atlassian took 15-20 years to reach ~$5B ARR. Anthropic is adding that every month. (Lenny).

-

Anthropic dominates Enterprise AI and that lead is accelerating. It now has 1,000 companies spending $1M+ each. A figure which doubled in under two months.

-

Anthropic by having the top AI coding model displayed around 1000% CAGR over the last 2.5 years.

Visualize It

The revenue growth at both Anthropic and Cursor demonstrate that vibe-working might have a sustainable future. Curiously OpenAI, Google and neither Microsoft or Meta are really in the picture. Anthropic’s Enterprise AI revenue began to step up just as their coding models have.

I think it was Claude 3.5 Sonnet that changed everything and established Anthropic as SOTA in coding. A bigger impact that even GPT-4 if you look at it historically many years from now. By the time Opus 4.0 was released, Claude Code was released in May, 2025 and Claude Cowork in January, 2026.

SOTA Opus Models, Claude Code and Claude Cowork changed everything. Who even knows what Mythos can unlock?

Sam Altman Exposé Goes Viral

New Yorker bombshell exposes OpenAI’s Sam Altman as untrustworthy manipulator.

Why read this? The New Yorker published an 18-month investigation into Sam Altman. The conclusion, from his own former leaders: he cannot be trusted.

Not news to us, but with looming IPOs it’s a problem for the AI ecosystem and AI bubble. OpenAI needs to change leadership, or risk everything! Both Sam Altman and Elon Musk are reputational risks to their companies now.

AI and Jobs

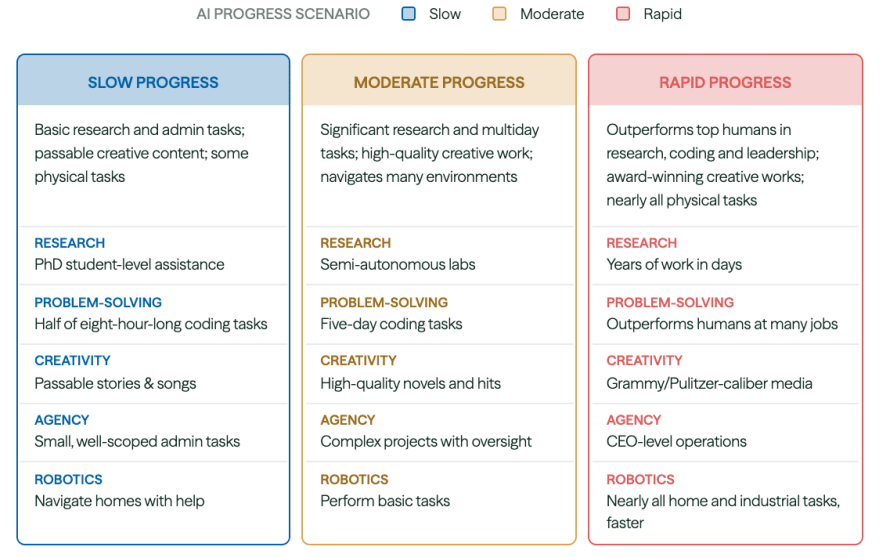

The Forecasting Research Institute completed what they call the most comprehensive study of how economists and AI experts think AI will affect the U.S. economy.

A majority of respondents anticipate significant advances in AI capabilities by 2030 with relatively stable historical trends for jobs and the labor market. That is, they predict major AI progress—but no dramatic break from economic trends in the next two decades: similar GDP growth rates to today, and a moderate decline in labor force participation.

What stood out to me? Labor Force Participation (LFPR): Under rapid progress, the LFPR is projected to drop from roughly 62% to 55% by 2050. Way more gradual than more biased economic reports insinuate.

Average Probability of AI Scenarios by 2030

I like how they modeled things: (although still a bit skewed to the Tech optimistic side). Nearly everyone is skewed to the AI optimism side now.

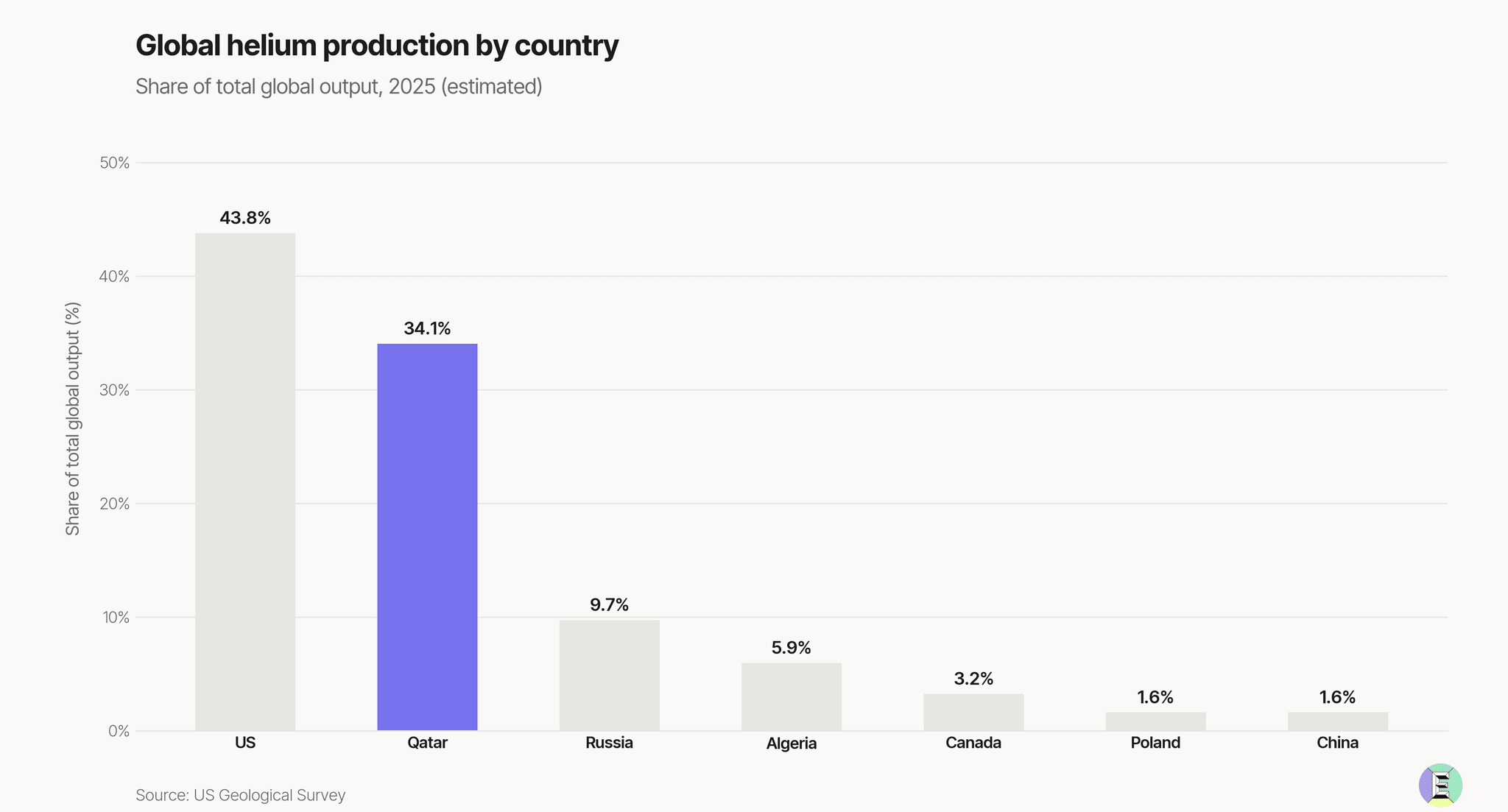

Helium Strait of Hormuz Bottleneck Intensifies

This is awkward?

-

Helium prices have skyrocketed since the start of the Iran war.

-

Qatar, which supplies a third of the world’s helium, has had production disrupted.

-

Helium is a critical input for industries like semiconductors, healthcare, and aerospace.

This so-called cease-fire notwithstanding, Helium’s impact to the semiconductor supply-chains is causing HBM prices to rise suddenly faster.

The semiconductor, medical-imaging, and aerospace sectors all rely on helium as a crucial component.

A third of the world’s helium is (was?) trapped. Qatar is the source of 34% of global helium supply. I’m fairly pessimistic about Trump’s ability to get a deal done with Iran and consider the Iran war a major threat to the AI bubble.

-

Helium prices are skyrocketing: early reports cited a 50% spike in the early going of the war, while more recent estimates say helium has doubled since late February.

-

Helium is as far as the Iran War and the semiconductor supply chain goes: as close to a “fundamental physical constraint” as we can get.

-

Qatar Energy announced in March it was halting production of liquefied natural gas and “associated products” following attacks on its facilities in Ras Laffan and Mesaieed. A 2-week ceasefire doesn’t change this, or anytime soon.

OpenAI over-invested in Compute and have a mediocre path to profitability

Even with compute success stories that bleeds cash OpenAI and xAI (SpaceX) are struggling to keep up with the superior AI talent at Anthropic.

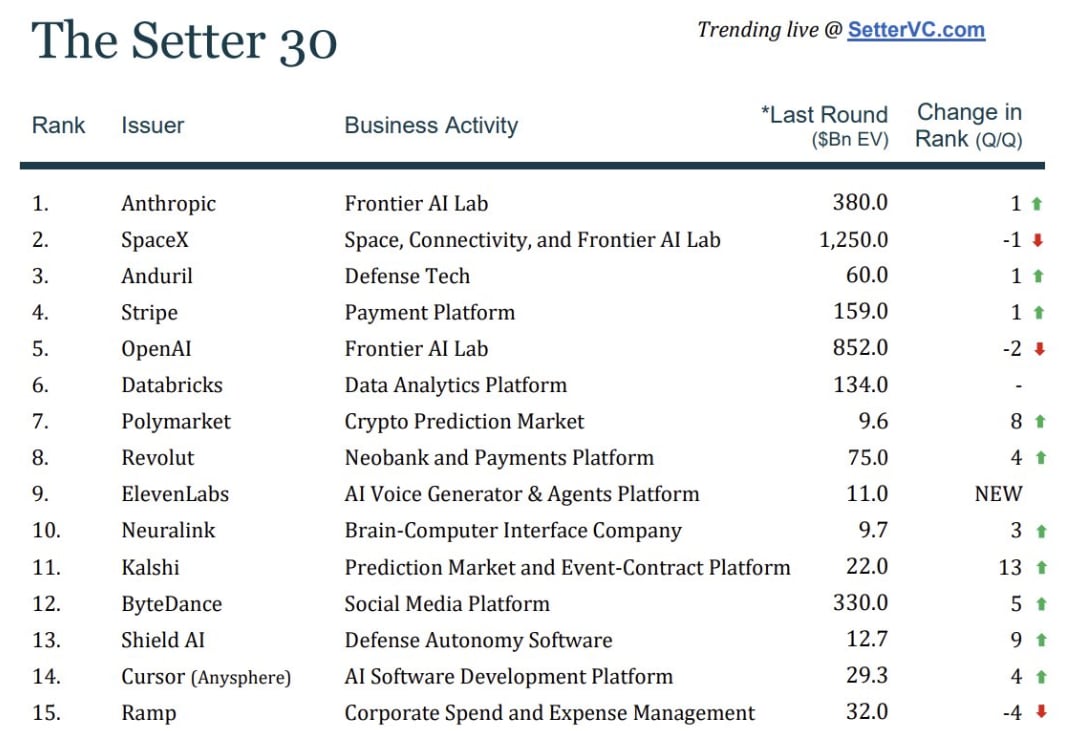

Anthropic is the hottest IPO in terms of Demand

Are you wondering why everyone is writing about Claude? It has to do with money.

As of April, 2026 these are the 30 most in-demand startup secondary shares in Q1 ’26 (per Setter Capital).

-

⬇️ OpenAI is falling

-

↗️ Anthropic is now in the top spot.

-

✨ Cursor is also quickly rising.

-

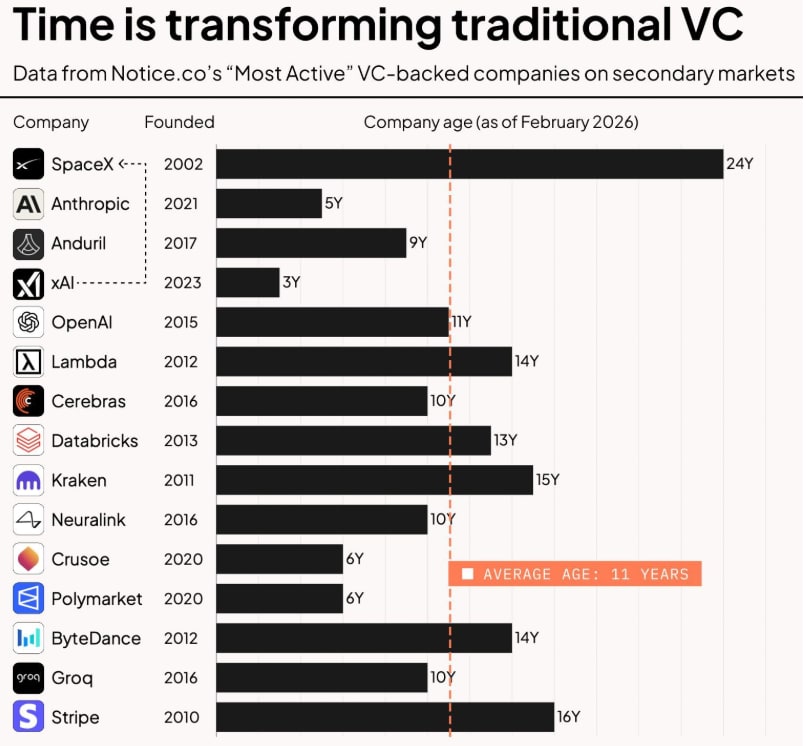

Five of the top six companies are big IPO candidates in the next 12-18 months.

I expect Blue Origin and Cursor to have to rush to an IPO in 2027 or 2028.

In BigTech historically Facebook IPO’d at 8 years. Google at 6 and Apple at 4.5. Private markets took a turn, in years remember that now Stripe is 16. Databricks is 13. Kraken is 15. SpaceX is 24. These aren’t startups any longer, these are mature well funded companies that have grown ARR fairly well. The 2026-2027 IPO year compresses time.

The 2026 Datacenter Delay Crunch

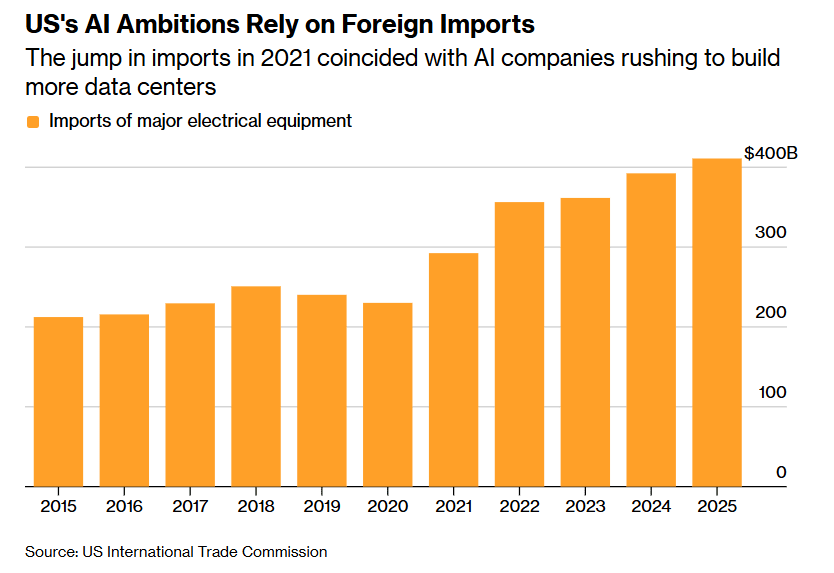

Bloomberg reported this week that half of planned US data centers are now delayed or canceled.

While the headlines focus on the capital being poured into AI, the physical reality of construction is hitting a wall. I’m sort of getting obsessed with the long list of such bottlenecks (or chokepoints), we covered it here already to some extent. Curiously this is getting hardly any media attention, like a censorship blackout.

-

Greater number of U.S. states in legal limbo due to community protests and local concerns.

-

Rise in HBM memory chips, made worse by the Helium shortage.

-

Supply-chain delays due to Chinese parts and Transformer crunch. That is, Transformers, switchgear, batteries, and related power infrastructure are in severe short supply.

-

Energy, permit delays and regulatory processes backlogs

-

Despite reshoring efforts, the U.S. is still heavily dependent on imports for this hardware. Imports of high-power transformers from China surged from 1,500 units in 2022 to over 8,000 units in 2025.

-

Geopolitics: The Iran War has exacerbated the situation by driving up energy costs and disrupting global shipping routes for heavy equipment.

-

Operation Epic Fury but for AI chips. Geopolitical conflict in the Middle East has created a “quiet crisis” for the hardware side of data centers involving Helium like I have mentioned.

-

The 12 GW gap: Utilities and grids are strained by surging AI demand (data centers planned for 2026 could need ~12+ GW in the U.S. alone).

Even with significant Capital investment (capex): nearly half of all planned U.S. data center projects have been delayed or canceled.

The Human Cost

-

Growing community pushback over noise, water usage, energy costs, land use, and environmental impacts has led to moratoriums, rezoning denials, and cancellations (e.g., projects worth billions blocked).

-

Several U.S. states are literally pausing Datacenter roll-outs.

-

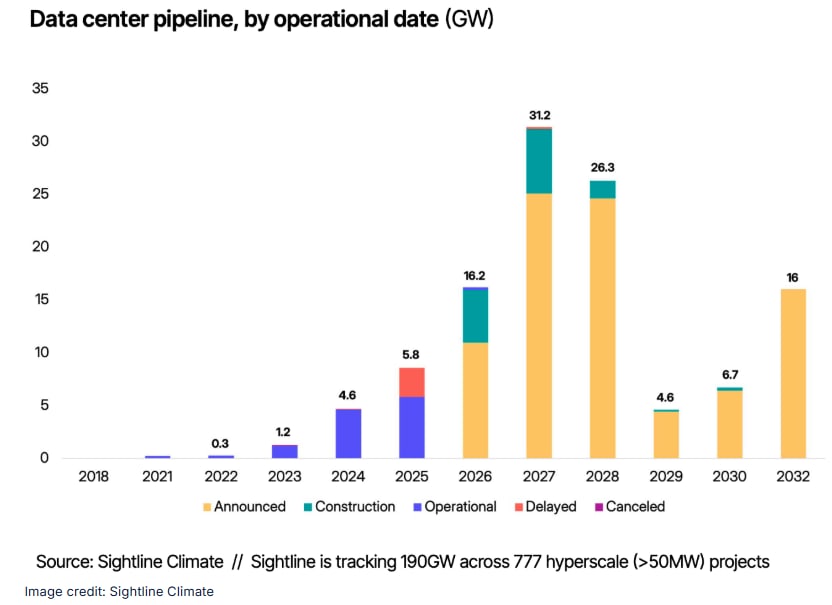

That’s a lot of Capex going up in smoke and the future looks pretty capacity constrained. This stuff is harder to build than we thought. The crazy part? Less than a third of the data centers originally scheduled to be operational by 2026 are actually under construction.

Supply chains are humbling the AI boom before we even have the courage to admit as a civilization that this is happening.

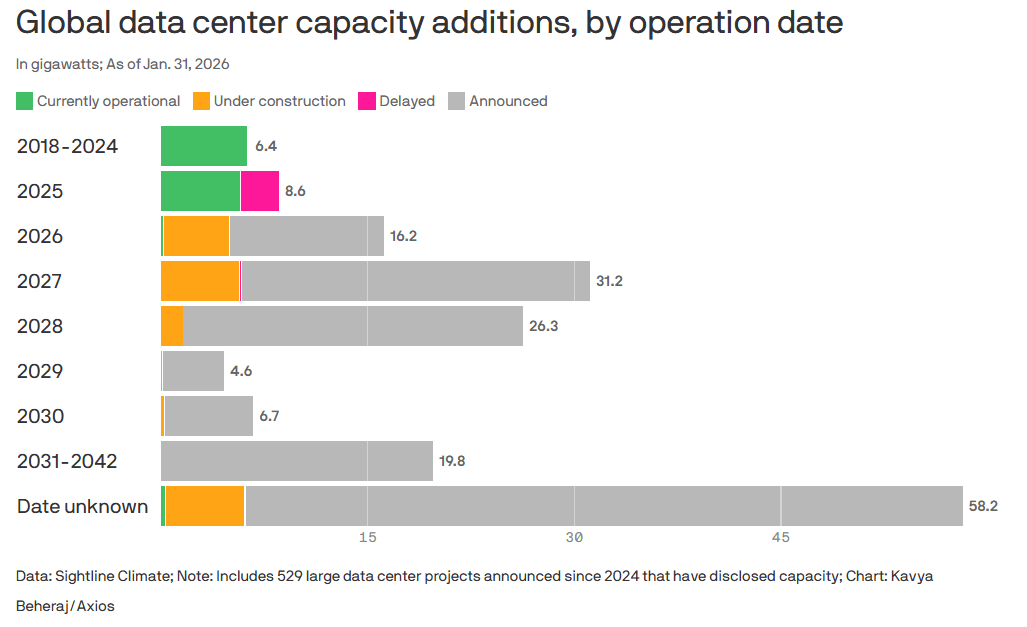

Between 30% and 50% of large data centers scheduled to come online this year are expected to be delayed due to power constraints, equipment shortages, and local opposition, according to new research by Sightline Climate (the Report of Feb, 2026 is about 18 PDF pages).

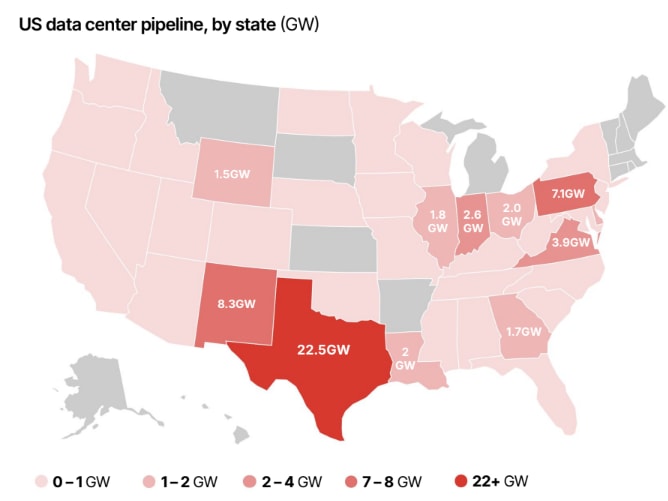

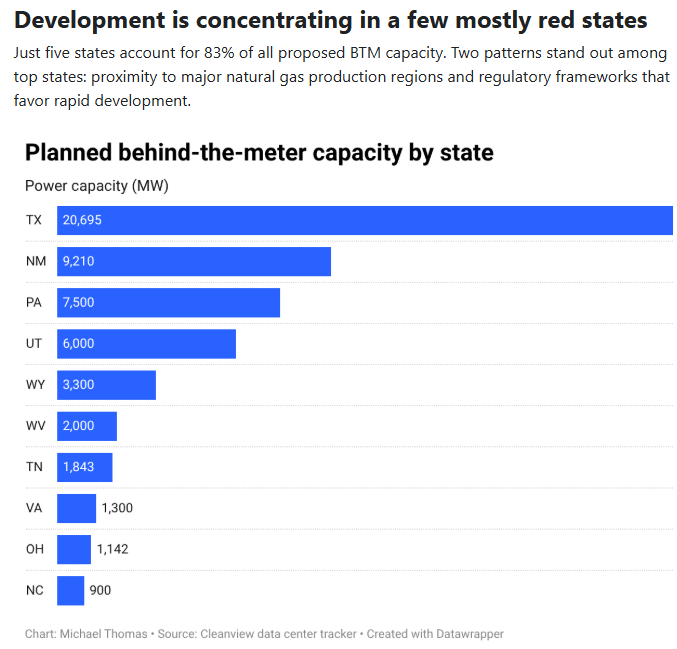

Texas, building the body of the “Machine Economy”

With more than 22GW of planned capacity, Texas leads US buildout. Its dominance comes from the promise of fast interconnection timelines, abundant generation, and a developer-friendly market structure, but the region is already seeing signs of strain with six projects delayed from 2025.

A Lot of Unknowns – the Uncertain Future of AI Datacenter Projects

-

A lot of “announced” projects are in execution risk limbo.

It’s a sign of mounting collisions in the AI race — from power constraints and grid equipment shortages to rising community opposition. – Axios

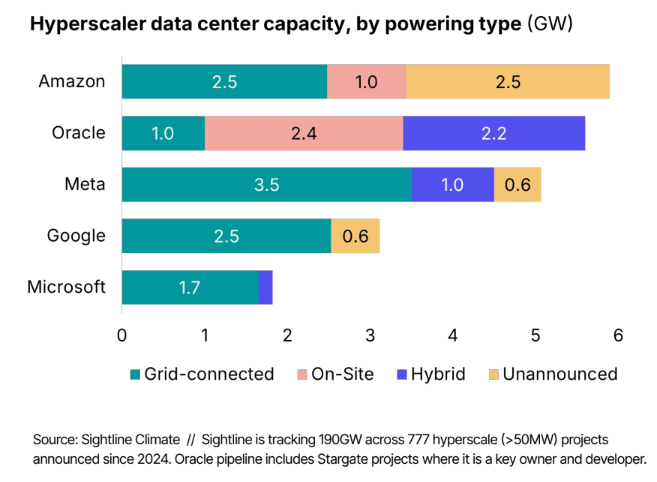

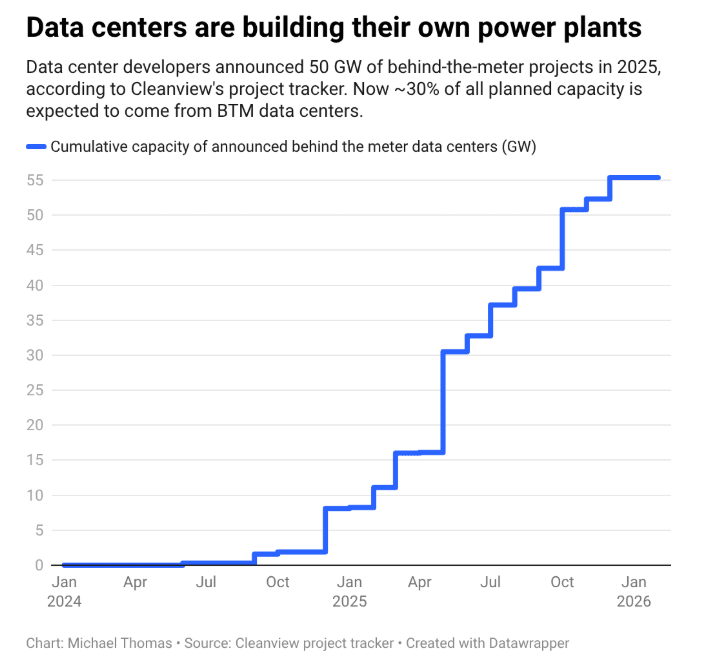

The result of these bottlenecks? Hyperscalers are giving up on the grid for AI training capacity. For example, Google parent Alphabet is acquiring Intersect, a data center company, for $4.75 billion in cash and the assumption of debt to speed up power generation. Bring your own Power. That makes AI Infra even more costly.

How ridiculous have things become due to wait-times?

Lead times for high-power transformers in the US stretched from 24 months pre-2020 to five years today.

-

5 years?

-

Most cannot afford to go off-grid power wise.

Talent Bottleneck in the Great AI Infra Slowdown of 2026

-

Nobody is talking about the talent and labor bottlenecks for the Great AI Infra slowdown. Labor/talent shortages: Skilled workers for construction and operations are in high demand; estimates suggest hundreds of thousands of unfilled positions.

The U.S. Needs to 7x output its Power/Energy Grid in the Next 15 years

But can it do it? The demand for compute is going to outsrip everything. . AI data center deployment cycles run under 18 months. The math doesn’t work. Logistics and delays are making more projects fail.

-

In the past 15 years, the U.S. added ~285 terawatt-hours (TWh) to the grid.

-

In the next 15 years, we’ll need ~2,000 TWh more (driven mainly by AI data centers, industrial electrification, and EVs).

It makes no sense. Not all the Capex in the world can solve these issues in a timely fashion. The promises vs. the reality completely break down when it comes to future compute and capacity required. What ends up happening? Rising costs and economic uncertainty leading some projects to be scaled back or deferred. Many will be cancelled. As I’m sure you realize, Electrical infrastructure represents less than 10% of total data center cost, but it is as vital as compute hardware. A delay in any single element of the power chain can halt the entire project.

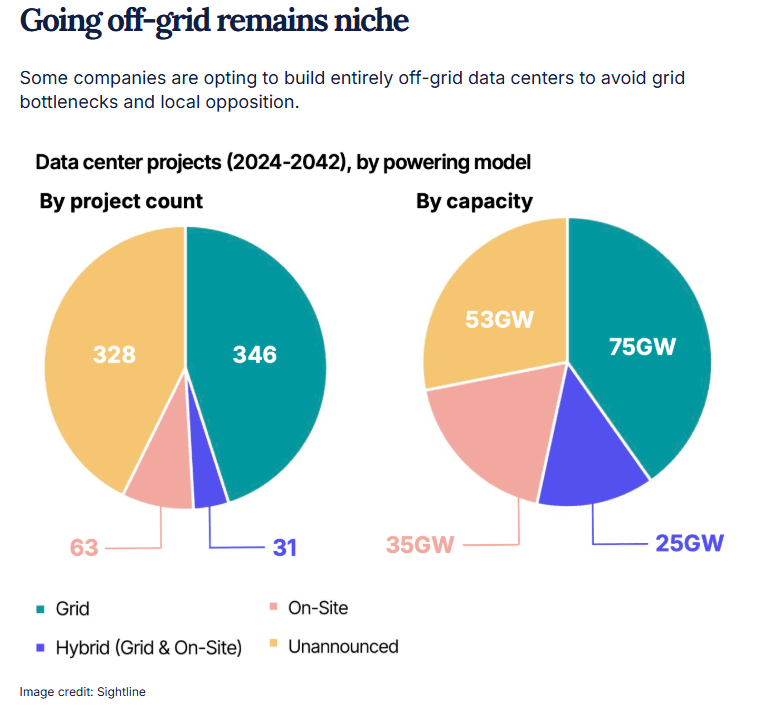

The Transition to On-site Power is going to be Rough 😬

Roughly 30% of all planned data center power capacity is expected to be on-site, according to a February report by Cleanview, a market intelligence firm — up from almost nothing a year earlier. This will add to costs considerably, increasing the debt of Neo Clouds, for example.

In a World where Speed Matters ⚡

Companies building AI infrastructure say avoiding the grid — at least initially — can bypass years-long waits to connect, provide more control and avoid straining the electric system with massive new demand (Axios).

The impact of the Iran War on the AI bubble and AI boom is even more complicated, which I have been thinking about a lot. An energy crisis Tsunami that is coming, will impact Political Sentiment around Hyperscalers, AI giants and Generative AI profiteering as a whole. This is the point where the affordability crisis comes head to head with AI for the 2028 Presidential Elections (closer than you think after November).

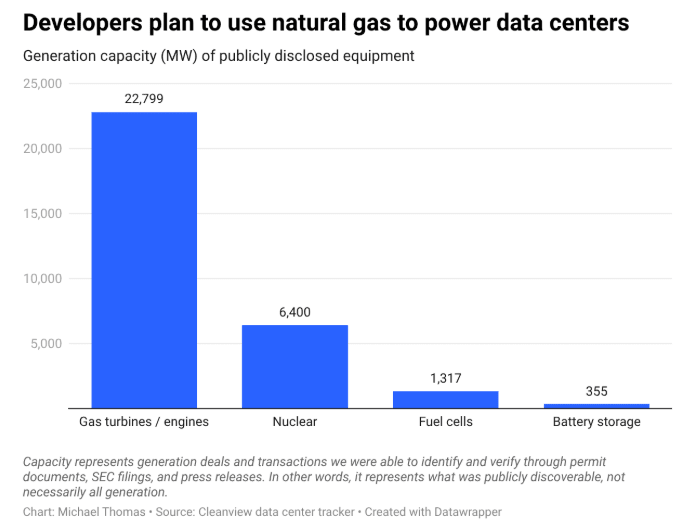

A Damn Dirty “AI Bridge”😵

The result? The shift toward natural gas as a primary, on-site power source for AI data centers has accelerated significantly in early 2026. This trend—often called the “AI Bridge”—is a direct response to the massive grid-interconnection delays (often 4–7 years) and the surging power requirements of H100/B200-class clusters.

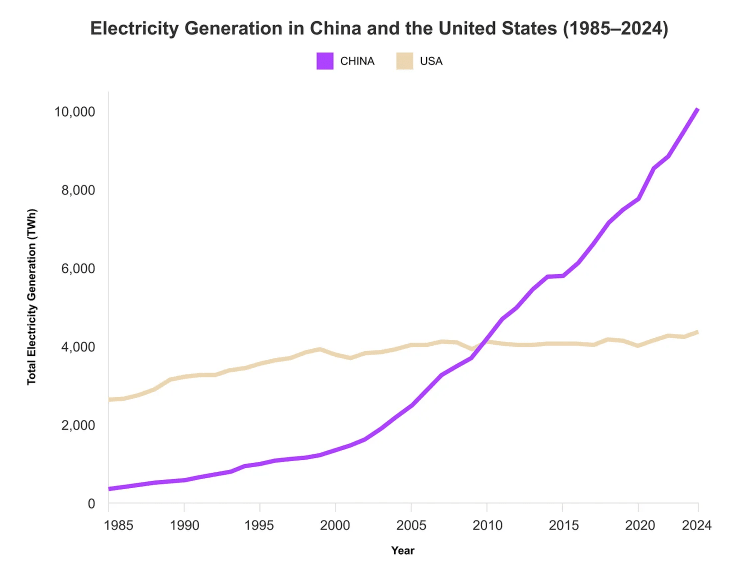

China has Overtaken the U.S. in Energy by a Wide Margin

I expect China to do the same in Space-tech harvesting of lunar bases and the Solar system in the decades ahead. Giving it an insurmountable Energy supremacy. If China is building nearly good enough models with a fraction of the capital and much worse GPUs, what will they be able to build when they reach semiconductor parity? (Honest Question).

America’s Desperation for Energy

While American consumers watch energy utility bills rise sharply.

The likes of Elon Musk’s xAI has popularity quick and dirty power for AI compute:

-

Mobile gas generators strapped to semitrucks

-

Aeroderivative turbines originally designed for aircraft and warships

-

Reciprocating engines that ramp fast, but are less efficient

-

Refurbished turbines acquired from industrial operations

Just the total opposite of clean or sustainable power.

U.S. Natural Gas Solution

Nothing like no environmental controls to push an AI agenda fast: while natural gas is “cleaner” than coal, it is increasingly viewed as “dirty” relative to the net-zero targets that AI companies previously committed to. Hyperscalers are abandoning their pledges (as politically it becomes optimal to do so).

Red States Rule for AI Datacenters

AI Datacenter Project Failures Rates will Spike in the 2026 to 2029 period.

Bottom line:

Only a fraction of 2026ʼs giant pipeline is under construction, making much of it unlikely to come online.

I find this all pretty wild compared to the lack of coverage due to its importance for IPOs like OpenAI, Anthropic and xAI related SpaceX.

Due to the rising demand for compute that I believe is exponential, I believe this will make “Neo Clouds” even more valuable due to the capacity constraints.

Addendum

These are some more field notes that you may be interested in skimming, reading or viewing.

Predictive History Joins Substack

The Viral “Professor” Jiang (Jiang Xueqin) has joined Subtack, I wasn’t even aware. This is his YouTube. He’s not a real Professor and he also has ideas on the AI bubble and AI datacenters as a “ponzi scheme”. He’s sometimes called the “China’s Nostradamus” and it’s not clear what’s tied to his rise to internet fame in recent months. I’m fairly aware of AI bears, so it’s surprising to me I wasn’t aware of his work before.

-

Jiang Xueqin is a Yale-educated educator and writer.

-

While he writes more on Geopolitics and American decline, his thoughts on the AI bubble do interest me.

-

He argues the U.S. economy is currently a “financial Ponzi scheme” propped up entirely by AI investments in data centers.

-

Much of this AI capital comes from Gulf State petrodollars. If the war in the Middle East disrupts energy infrastructure (desalination plants or the Strait of Hormuz), the Gulf States will stop recycling dollars into U.S. tech.

-

In his estimation (prediction?), this will result in a catastrophic burst of the AI bubble, which he claims will trigger a wider collapse of the American financial system.

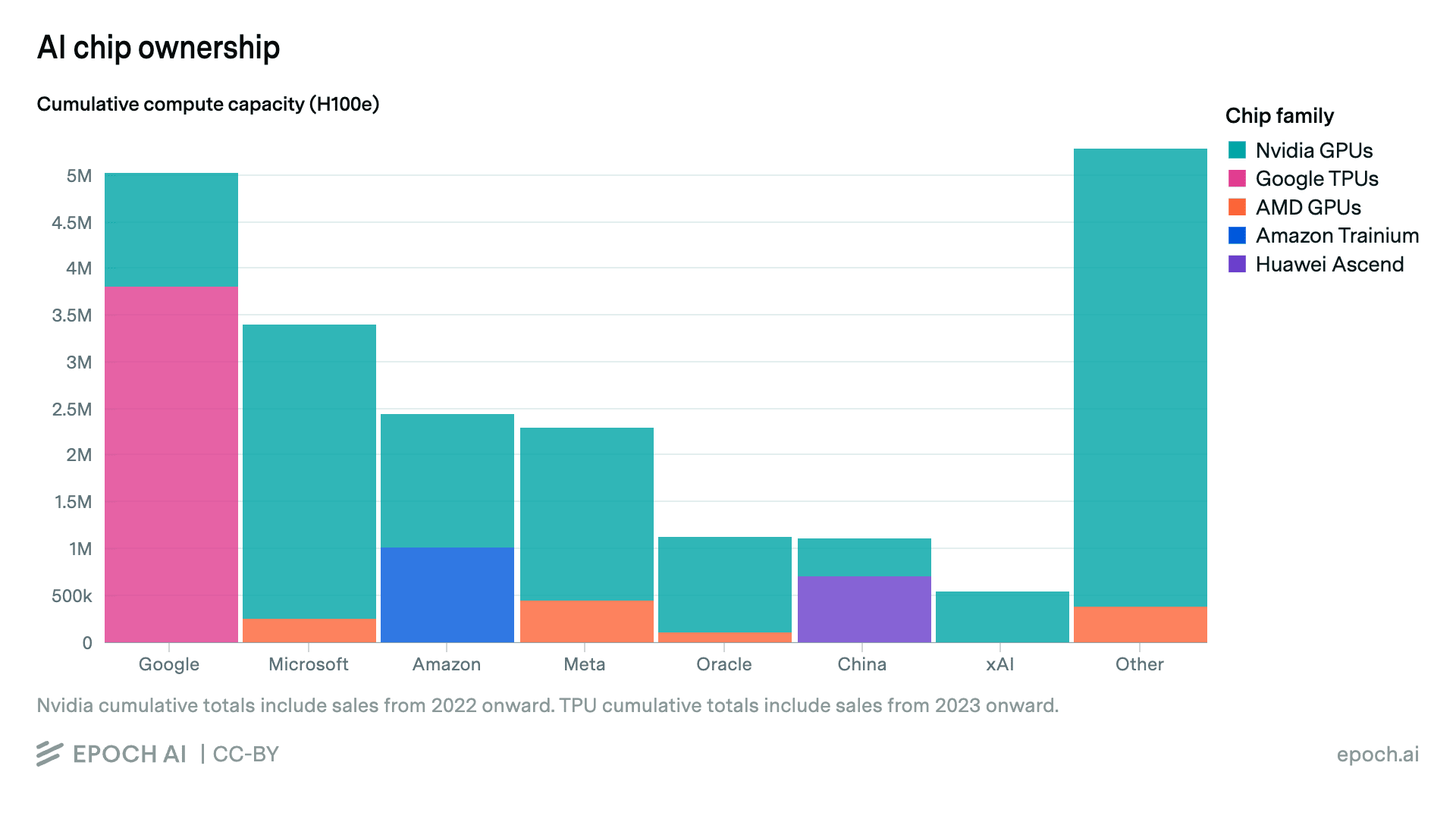

Who Owns the Compute or at least the GPUs Historically Speaking

-

Epoch AI claims China owns just 5% of global compute.

Generative AI Hype Unlocked Compressed Time to Innovate

Department of War-esque and American Dynamism-esque startups like Anduril, Shield AI, Crusoe, Polymarket and Anysphere bring backs the rush to IPO as huge liquidity on the sidelines. (Founders Fund & a16z are key funds to watch]. OpenAI goes public right on schedule but unfortunately before its valley of death. Confidence in OpenAI is decreasing rapidly in 2026.

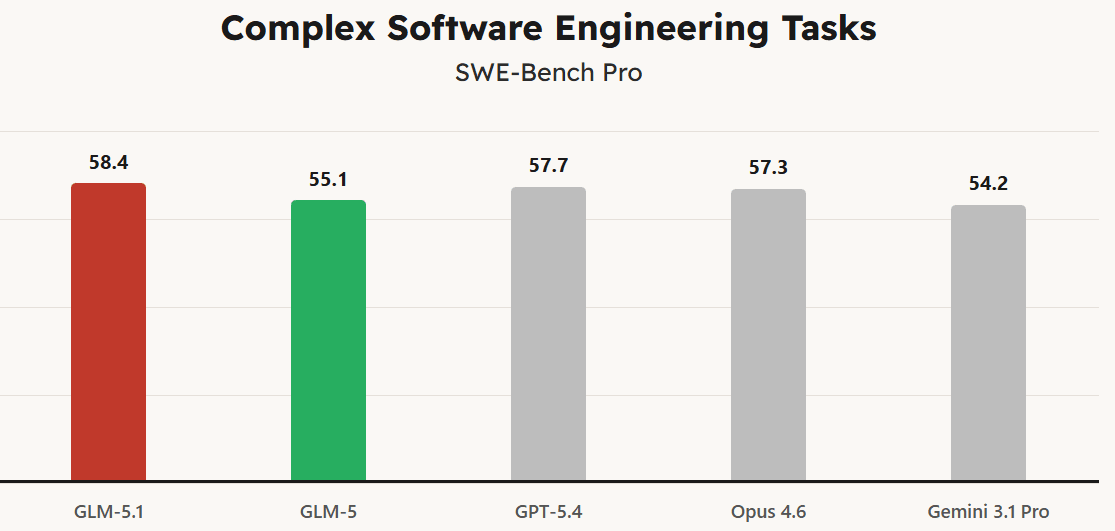

Zhipu AI released GLM-5.1: “The Next Level of Open Source”

It’s a rather important model after Qwen’s pivot – Alibaba has restructured its AI operations under the “Alibaba Token Hub” (ATH) with a clear mandate to turn AI into a recurring revenue engine. Zhipu AI (now frequently branding as Z.ai following their January 2026 IPO) has been extremely active in 2026. GLM-5.1 is a 754-billion parameter Mixture-of-Experts model engineered to maintain goal alignment over extended execution traces that span thousands of tool calls.

Zhipu claims a score of 94.8 on the Design2Code benchmark, notably higher than many Western frontier models in the same category. So instead of being 9 months behind U.S. models as in 2025, China is now about 3 months behind closed models and maybe six months ahead in open-weight models and what U.S. startups typically build upon.

China has a greater number of frontier AI labs and startups than the U.S. does that are building world class LLMs. It is also claimed that Z’s GLM 5.1 is the first frontier-tier model trained entirely on domestic Huawei Ascend 910B clusters, rather than Nvidia hardware. Good luck trying to verify that.

Don’t Forget South Korea

By 2027, Samsung is expected to have the largest operating profit of any company in the world, per Jeffries. SK Hynix is a big riser as well.

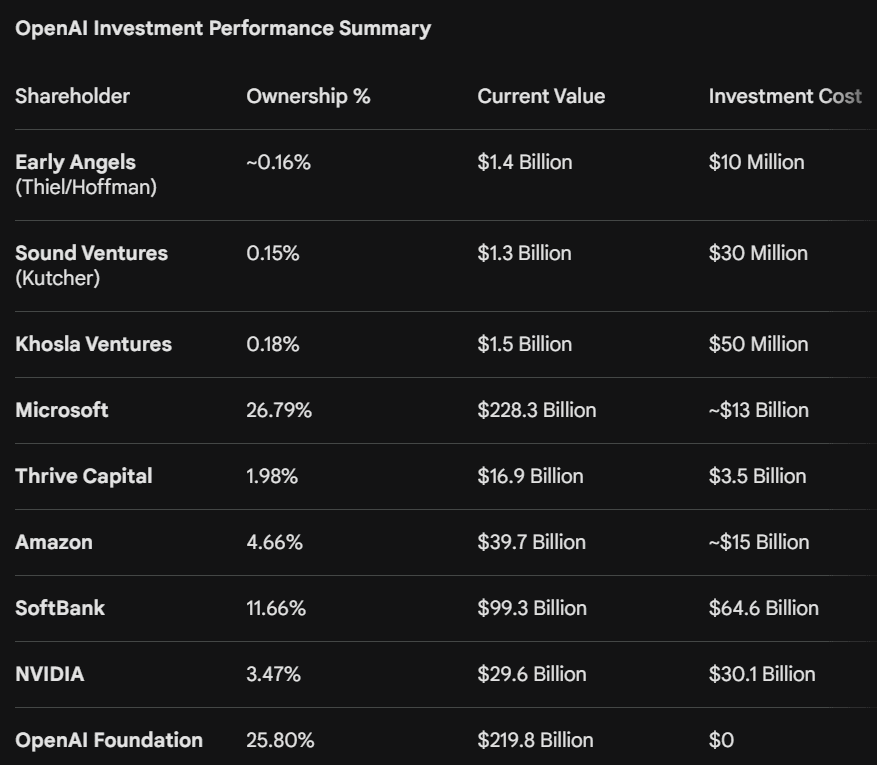

OpenAI’s estimated cap table leak

The leaked OpenAI cap table from early April 2026 highlights the massive valuation gap between early-stage backers and late-comers.

-

Microsoft put in ~$13B. Now worth $228B. 17.6x return on the single largest corporate AI bet ever made.

-

SoftBank committed $64.6B for 11.66%. Already sitting on ~$50B in unrealized gains. But at a blended 1.5x, that’s not even a good fund return for the size of the check.

-

NVIDIA holds 3.47%, valued at $29.6B, against a cost basis of $30.1B. The “picks and shovels” play is at 1.0x. A big chunk was in-kind GPU credits, not cash, so the real economics are murkier.

-

Early angels are at ~140x. Sound Ventures (Ashton Kutcher’s fund) turned roughly $30M into $1.3B. Khosla is at 30x on a $50M check.

Somehow the Non-Profit Foundation now only holds one fourth of the company.

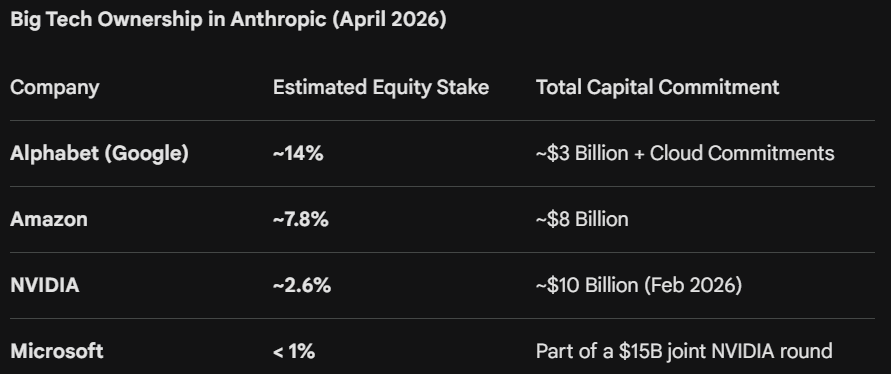

Anthropic Estimated Cap Table BigTech Shares

Now Google has the biggest equity stake in Anthropic among the hyperscalers with significant partnerships. Anthropic signed a new agreement in April, 2026 with Google and Broadcom for multiple gigawatts of next-generation TPU capacity that we expect to come online starting in 2027.

-

Nvidia holds a 6% stake in BigAI.

-

Microsoft still owns approximately 27% of OpenAI, making a 17x return from the initial investment.

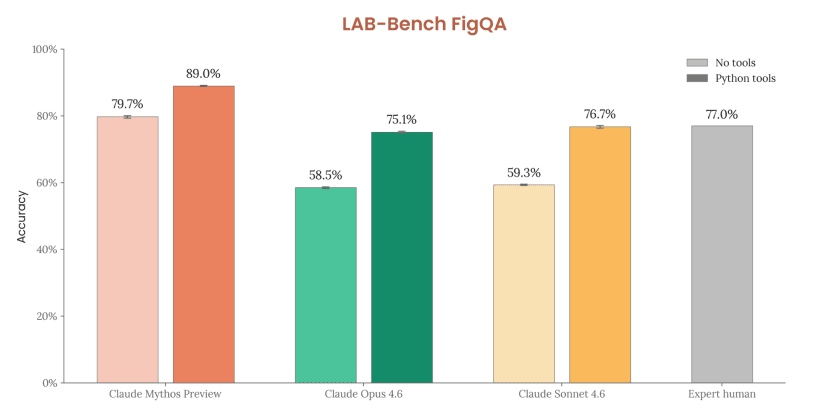

Mythos Lab-Bench Benchmarks

Page 193 of System Card Preview: LAB-Bench FigQA is a visual reasoning benchmark that tests whether models can correctly interpret and analyze information from complex scientific figures found in biology research papers.

Is Claude Mythos going to be insanely Token Efficient?

Anyways I’ve run out of time, there are a lot of other points I wanted to cover.

Read More in AI Supremacy